1. Capped Supply (21M) vs. Millionaires

UBS puts the number of dollar millionaires in the United States at roughly 24 million. Globally, the figure approaches 60 million. There will only ever be 21 million bitcoin.

About 20 million have been mined so far, and industry estimates suggest 2.3-3.7 million of those are permanently inaccessible — lost to forgotten keys, destroyed hardware, and dead owners.

Of the remaining ~16-17 million accessible coins, long-term holders (addresses holding 155+ days) control roughly 75-80% of circulating supply. Only about 2.3 million BTC currently sits on exchanges — roughly 12% of supply, down from 3.1 million in 2020. The liquid free float is a fraction of the headline number and it’s shrinking.

Meanwhile, new supply is collapsing. The April 2024 halving cut the block reward to 3.125 BTC — only about 450 new coins per day, or ~164,000 per year. The next halving (~2028) cuts that in half again. Since the April 2024 halving, Bitcoin’s inflation rate (~0.85%) is now below gold’s (~1.5%) for the first time in its history.

Even if only the world’s millionaires each wanted a single coin, the majority couldn’t get one. Add sovereign wealth funds, corporate treasuries, pension funds, ETFs, and tens of millions of existing fractional holders.

Whole-coin ownership is already arithmetically scarce, and that scarcity tightens on both sides — existing supply is locked up by holders, and new supply is cut with halvings. The window for whole-coin accumulation is closing, and it won’t reopen.

The current case for owning bitcoin is less about upside speculation and more about the increasing irrationality of holding zero exposure.

2. Debt-to-GDP Ratio

Total public debt outstanding stood at approximately $38.9 trillion as of early March 2026. CBO’s latest projections put debt held by the public at 101% of GDP — the highest since World War II.

Net interest outlays hit $970 billion in fiscal year 2025, surpassing defense spending ($919 billion). CBO projects interest will exceed $1 trillion this fiscal year, consume nearly one-fifth of all federal spending by 2036 (120% debt-to-GDP), and reach 175% by 2056.

The spiral is reflexive:

Higher debt → Higher interest → Wider deficit → More borrowing → More debt.

The U.S. is running structural deficits near 5.8% of GDP during expansion — the phase when deficits are supposed to shrink. CBO projects 6.7% by 2036. Next recession, we start from 101% debt-to-GDP, not the 35% of 2008 or the 79% of 2020.

There is no political coalition for austerity. The debt-to-GDP ratio can only be managed through nominal GDP growth that outpaces borrowing costs, which requires the Fed to keep real rates negative or near-zero for extended periods. That’s the revealed preference of every sovereign debtor in history once they cross the threshold the U.S. crossed around 2020.

If the dollar must be debased to keep the sovereign solvent, then anything denominated in dollars is melting. Your savings account, bond allocation, and cash position are slow-motion short positions against the unit of account itself.

The dollar need not lose reserve currency status for the bitcoin thesis to work. In fact, the U.S. dollar is very likely to remain the world’s reserve currency given dollar-denominated trade, stablecoins, contracts, and debt.

But reserve currency status and purchasing power are not the same thing. The dollar has lost over 97% of its purchasing power since 1913 while maintaining reserve currency status the entire time. Reserve status means the world uses dollars but it doesn’t mean the world trusts dollars as a store of value.

That’s why central banks have been accumulating gold at the fastest pace in decades — diversifying away from the dollar as a store of value, not abandoning it as a medium of exchange.

3. Debasement Accelerates: The Demographic-Electoral Ratchet

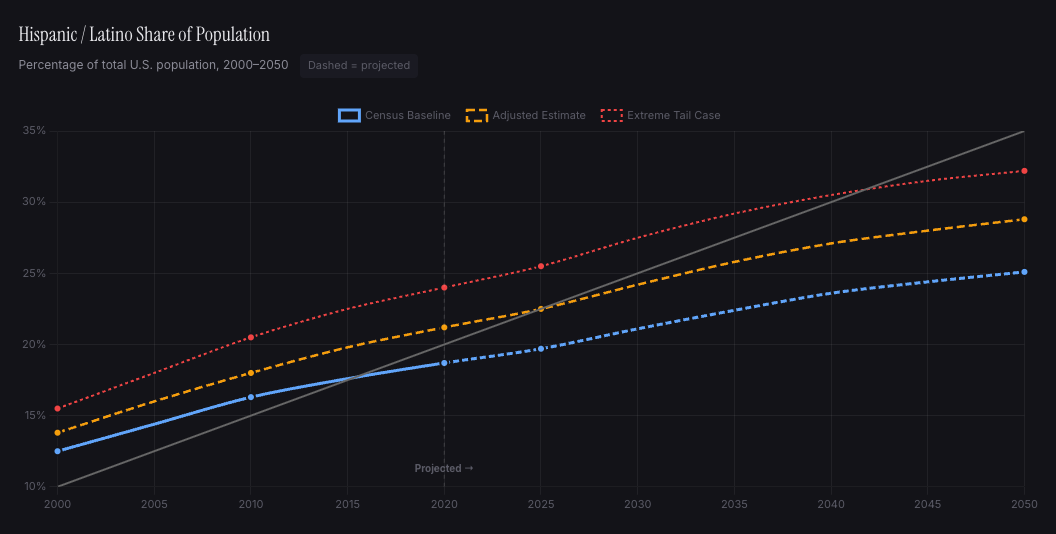

The U.S. electorate is undergoing a compositional shift that is a one-way conveyor belt toward a larger, more fiscally expansionary state. Hispanics are the fastest-growing demographic bloc and have revealed consistent preferences across the global Hispanic diaspora and within the U.S. whenever they become majority (e.g. California).

Political commentary misleadingly frames the Hispanic vote as left vs. right. It isn’t. On fiscal questions: redistribution, welfare, government services, healthcare, education spending — Hispanic voters on both sides of the aisle consistently favor a larger, more active government; this is true for all age brackets.

This is why the growing Hispanic share of the electorate is structurally disastrous for fiscal conservatism regardless of which party captures those votes.

Republicans win them by catering to short-term populist impulses (tariffs, industrial policy, family tax credits, border spending, larger government, social conservatism) — which is precisely why the party has become more populist/nationalist.

Democrats win them by catering to immediate gratification, envy impulses (Elon Musk has more money than you! He doesn’t deserve it! You and your family are struggling and he owes you!), and socialism (everything is a human right! free housing! rent control! free unlimited advanced healthcare!). The playbook is tax the rich, target the billionaires, give more handouts, etc.

As the “legal” Hispanic citizen share rises from ~20% today to 30%+ by mid-century, the median voter on fiscal questions drifts steadily toward a larger state. The slow drift toward a permanently blue fiscal consensus (even if the cultural map stays purple) is the reality both parties are adapting to, not fighting.

By 2045, the U.S. is majority-minority. This isn’t even contingent on immigration policy. Median age of White Americans: ~44. Median age of Hispanic Americans: ~30 — and the birth rates are higher among Hispanics There is no electoral coalition for austerity.

Furthermore Hispanics as a group are likely, based on best estimates (accounting for off-the-books tax avoidance, crime, net extractions at all level of government, etc.) lifetime NPV negative.

The CATO Institute is notorious for pushing propaganda “immigration boosts GDP” — including illegal immigration! CATO lacks objective NPV data so they use methodologically dishonest “survey modeling” without accurately adjusting for: off-the-books jobs with no taxation, multi-gen voting behavior (socialism/redistribution), public benefits usage (state, local, federal, charity, NGO, etc.), displaced native-born American workers, slower transition to automation, etc.

And we have an entitlements problem that grows larger by the day. The 2025 OASDI Trustees Report shows about 2.7 covered workers per Social Security beneficiary in 2024, projected to fall to 2.3 by 2040. Combined Social Security and Medicare costs will rise from 9.2% of GDP in 2025 to 12.1% by 2049.

Many low IQs have been psyopped into blaming the “Boomers” for the country’s fiscal woes instead of the U.S. gov spending like a manic zombie on a compulsive shopping spree.

“Boomer” beneficiaries were never the problem — they paid in far more what they will ever hope to receive and the U.S. gov found a million ways to blow it. The resulting $78 trillion 75-year shortfall estimated by Treasury’s 2024 Financial Report is chronic government mismanagement and irresponsibility.

The monetary debasement trajectory is an entrenched regime that is no longer cyclical. “Democracy” is functioning exactly as designed. Voters are getting what they want… and what they want requires the printing press; the effect: USD devaluation.

4. Mechanism: Bitcoin as a Global Liquidity Barometer

Lyn Alden and Sam Callahan’s research found that bitcoin moves in the same direction as dollar-denominated global M2 83% of the time over any given 12-month period — the highest directional consistency of any major asset class tested. Overall correlation from 2013 to 2024: 0.94. Why bitcoin? No earnings, dividends, structural 401(k) bid, countercyclical safety bid. It’s what Alden calls a “pure liquidity barometer.”

My updated research with GPT-5.4-Pro through January 2026 found the correlation weakens on a same-month basis but improves when liquidity leads bitcoin by roughly 1-3 months. The signal is a medium-term state variable — not something for day-trading.

Every major central bank operates under the same constraints: over-indebted sovereigns, deteriorating demographics, political systems that cannot tolerate austerity. Dollar-denominated global M2 went from ~$80 trillion in 2020 to past $105 trillion. Brief counter-trend episodes get reversed by policy panic every time.

Bitcoin’s supply is completely unresponsive to this expansion.

This is the point the liquidity data is making: it doesn’t matter whether the next Fed cut is in June or September, or whether oil is at $70 or $95 this quarter. Those are noise on a multi-decade signal. Every central bank on earth is trapped in the same demographic and fiscal vise described above, and the only tool that works (monetary expansion) is the one tool that makes a fixed-supply asset more valuable over time.

Fixed supply against a structurally expanding monetary base.

5. The Trust Deficit Is Increasing

Fraud throughout the U.S. is so rampant it would take eons to uncover it all. Hard-working Americans have their wealth extracted by parasites while the government does nothing until a critical mass of social pressure surfaces. Your taxes are funding a vicious circle of fraud and NGO feedback loops.

Left-wing states don’t investigate unless mass-pressured by right-wing media and government — and we aren’t even scratching the surface of what’s happening in NY and CA. We wouldn’t have uncovered any of this if Republicans lost the last election.

Americans watched the government distribute trillions in COVID stimulus and act puzzled about inflation. SBA’s OIG estimated over $200 billion in potentially fraudulent PPP and EIDL disbursements. The Feeding Our Future case — just one detected scheme in one state — is now a $300 million+ fraud, and Minnesota alone has nearly $822 million in confirmed fraud across just three social programs.

California: $30 billion+ in potentially fraudulent unemployment claims. New York spends $115 billion a year on Medicaid — highest per capita in the nation — and just had a federal fraud probe launched after investigators found $2.6 billion in premiums paid for people who don’t even live in the state. GAO estimates the federal government loses between $233 billion and $521 billion annually to fraud across all programs, with Medicare and Medicaid alone accounting for over $100 billion in improper payments per year. Nobody pays a meaningful price for any of it.

The U.S. government may still do more good than harm, but many savers rationally prefer systems with fewer trusted intermediaries after what they’ve seen in the past 20 years.

Bitcoin doesn’t ask you to trust anyone. In a low-trust, high-fraud institutional environment, a zero-trust system is a rational response to reality.

6. Why Bitcoin Over Other Hard Assets

Gold remains the apex reserve asset and most smart people probably own some. But bitcoin has several properties gold doesn’t: (1) perfect portability, (2) rapid settlement, (3) cryptographic verifiability (no paper shares that don’t match actual supply in vaults), and (4) absolute supply inelasticity.

You might ask: Why not just own hard assets (e.g. gold, uranium, copper)? You probably should own some! But every physical commodity’s supply responds to price. When gold hits $3,000, marginal mines reopen. When uranium spikes, mothballed deposits get permitted. Supply curves bend. Bitcoin’s supply response to rising demand is mathematically zero.

Physical commodities also carry storage costs, counterparty risk, jurisdictional exposure — and governments can confiscate them. FDR seized private gold in 1933. Self-custodied bitcoin is far harder to confiscate — no physical object to seize, vault to raid, intermediary to subpoena; you can say you forgot your keys and nobody will know whether you really did or not!

Try walking through airport security with $100,000 in gold bars. Gold is excellent at being scarce; it fails on portability, concealability, and instant transferability. Bitcoin solves all three: your entire net worth in your head, across any border, to anyone with an internet connection in minutes.

The people who understand bitcoin most viscerally are Argentinians, Lebanese savers who watched their deposits get haircut 80%, Russian dissidents. For anyone whose threat model includes jurisdictional risk, bitcoin’s advantage over gold is substantial.

7. The Bitcoin HODLer Network Effect

Bitcoin has no CEO or marketing department. Every holder is an advocate because they’re financially incentivized to be one. The holder base is growing while the dollar’s credibility is shrinking.

U.S. spot bitcoin ETFs pulled in ~$37 billion in their first year. And an important dynamic is who’s selling — and what they’re saying. BlackRock, Fidelity, Invesco, and Franklin Templeton are actively pitching bitcoin as a unique portfolio diversifier — uncorrelated, no earnings dependency, supply immune to central bank policy.

When the largest asset managers in the U.S. tell clients a 1-2% bitcoin allocation improves portfolio efficiency, that’s the distribution machine of traditional finance pointed at an asset with a fixed supply of 21 million units. This demand is structural, recurring, and still in early innings.

The White House established a Strategic Bitcoin Reserve in March 2025 (forfeited BTC, budget-neutral). Bitcoin has crossed from taboo to policy-relevant. The most powerful government on earth treats it as worth holding, and the most powerful asset managers are telling clients to own it.

Important nuance: the institutional bull case and the sovereignty bull case are not identical. ETFs are bullish for price. Censorship-resistance applies to self-custodied bitcoin, not paper exposure. The strongest case involves both.

And you can’t replicate the network effect. Launching “Bitcoin 2” would be like launching “English 2.” Sixteen years of unbroken uptime, no rollbacks, no bailouts, no central authority, and a growing HODL’er network is the moat.

The strongest bear case is that governments could clamp down on on/off-ramps and render bitcoin effectively unusable. Two years ago this was a legitimate concern. Today the U.S. government holds a Strategic Bitcoin Reserve, BlackRock manages a bitcoin ETF with tens of billions in AUM, and both parties are competing to be more pro-crypto, not less.

The institutional distribution channel is both bullish for value appreciation and a good defense against regulatory kill shots. BlackRock and Fidelity didn’t spend billions building bitcoin products to watch them get banned.

To be honest about the tail risk: a future far-left administration could reverse the current position, dissolve the Strategic Reserve, shut down ETFs, and use FATCA-style pressure to force allied countries to dismantle on/off-ramps. The US proved with FATCA that it can bully the entire global financial system into compliance. That scenario wouldn’t kill the protocol — bitcoin would still function, P2P markets would still exist — but it could significantly damage bitcoin’s value and liquidity for years.

The reason I still think the probability is low and declining: the political coalition required to do it gets weaker every year as voter ownership expands, Wall Street’s revenue depends on the asset surviving. Every year bitcoin embeds deeper into the financial system, the reversal cost goes up.

8. Flight Optionality and the Eternal Ratchet

Washington state just passed a 9.9% income tax on earnings over $1 million. The same day, Howard Schultz (44 years in Seattle) announced he was leaving for Miami. Bezos already left after the capital gains tax. Starbucks is opening a corporate office in Nashville.

I predicted this long ago and it’ll only accelerate as the White population shrinks. The options with our new demographics are: Populism vs. Socialism — with significant overlap in fiscal preferences but disagreements in social ones.

California already has a 13.3% top marginal rate and just proposed 5% billionaire wealth tax on the November 2026 ballot. Pirate Wires spoke with 21 billionaires; nearly all including left-wingers are developing exit plans. 70% of a billionaire Signal chat said they’d leave if it passes, 15% already gone. Zuckerberg bought Indian Creek. Page, Brin, Thiel, Sacks — all relocating.

The ratchet never stops. Taxes go up. Regulations expand. Immigration increases. When was the last time a major Western government reduced its claims on private capital in a sustained, structural way?

All downstream of being too cowardly to confront reality:

Any “peer reviewed” academic and/or econ literature that’s against any of the following: (1) free markets, (2) more capitalism, (3) deregulation, (4) the deterministic impact of genetics — can be reflexively dismissed with zero thought; it contradicts human incentives, feedback loops, and observed reality + human history.

Wealth migration takes away jobs, slows/destroys innovation, etc. and does massive amounts of damage. Low IQ left-wing voter blocs want immediate gratification and don’t “learn lessons” after collapse — they just become Cuba and Venezuela and wait for federal bailouts or infinite collapse-rebirth cycles.

They’ve gotten the policies they wanted in the U.K., Europe, Canada, etc. and we can see what lower human capital combined with voting power does: more regulation, more socialism/redistribution, flight of the competent to other countries, more open borders/immigration, etc.

This is all a slow decline and Hail Mary prayer that the U.S. swoops in and saves them with AI/robotics and gene engineering.

Lower innovation rate gets blamed on stupid things like “well we got all the low hanging fruit” (without factoring in damage via regulatory handcuffs, higher taxes, and lower human capital — which could account for most of the observed modern-day innovation paradox).

If your country is slowly being bled dry by parasites, Bitcoin is one potential strategy by which you could efficiently relocate to a new country or jurisdiction with just a seed phrase. If wealthy Americans are already fleeing states, demand for a jurisdictionless store of value should increase (especially considering many states want to freeze assets before departure and/or retroactively claw your finances).

9. AI Does Not Obviously Kill Bitcoin

Three paths:

AI doesn’t diffuse efficiently. The fiscal mess continues, the demographic ratchet grinds forward, global liquidity keeps expanding, and the core debasement case for bitcoin stays fully intact. This is the scenario where bitcoin does best.

AI advances but bitcoin retains value. Even in a world of significant AI-driven productivity gains, bitcoin could retain value — possibly significant value. AI can produce anything informational and drive down the cost of physical goods, but it cannot produce more than 21 million bitcoin. A world saturated with infinitely replicable digital output may make credibly fixed digital scarcity more legible, not less. Bitcoin could function as a unique form of money in a future economy, a digital collector’s item with network effects, or the last truly scarce asset in an increasingly abundant world. If AI concentrates power into a few firms and states, censorship resistance and non-sovereign savings become more valuable, not less.

Full AGI abundance arrives but bitcoin goes to zero. You won’t care. If AI so thoroughly solves scarcity that a monetary hedge becomes worthless, you are living in a world of such profound abundance that the loss on your bitcoin position is meaningless. Your basic needs — and probably far more — are covered regardless.

A modest bitcoin allocation works across all three paths. The only scenario where it “hurts” is one where it doesn’t matter.

10. The Window

There is nothing magical about “1 BTC.” The financially intelligent question is bitcoin exposure relative to your net worth, time horizon, custody situation, staying power through volatility and perceived opportunity cost. Bitcoin’s drawdowns are severe — don’t size a position that would force you to sell.

But you don’t need a whole coin. Even a 1% portfolio allocation gives you asymmetric exposure to every structural force in this piece. If we’re wrong and bitcoin goes nowhere? You’ll probably never notice. If correct? Potentially the best performing allocation you’ve ever made. The downside is capped. The upside is not.

Bitcoin’s market cap is ~$1.4 trillion — roughly 4% of gold’s mid-$30-trillion valuation. Every incremental use case represents upside from here. The demographic, fiscal, political, and monetary forces above are all structural, all accelerating, all pointing the same direction.

Given everything we can clearly see coming, the question is whether you can afford zero exposure to the only natively digital, permissionless, fixed-supply monetary network in existence.

Closing note: Now doesn’t seem like a bad time to buy.