U.S. Steel x Nippon Steel Deal Blocked: Implications & Future Scenarios (2025-2030)

Blocking the sale of U.S. Steel to Nippon Steel (Japanese company) to protect domestic interests may have been dumb, but the U.S. could turn it into a win...

On January 3, 2025 Joe Biden blocked the acquisition of U.S. Steel by Japan’s Nippon Steel, citing national security concerns.

Negotiations had been ongoing since December 18, 2023 and lasted approximately ~1 year before the deal was shot down by the U.S. president (even though U.S. Steel is a private company – not a division of the U.S. government).

Would Trump have allowed the deal? Nope. He stated that through tax incentives and tariffs his admin would “Make U.S. Steel Great Again” and proposed: tax incentives to strengthen the company and tariffs to protect domestic steel production.

Trump issued a direct warning on social media: “Buyer Beware!!!” So this is a deal that U.S. Steel couldn’t have gotten done under either administration. In addition to Biden and Trump, the United Steelworkers Union wanted the deal blocked.

Although support for the blockade was unanimous and there are some legitimate reasons block the deal, there may have been more upside to allowing the deal to go through in terms of allowing free markets to thrive (U.S. Steel wanted to sell), selling to a company within an allied nation (Japan), and protecting jobs (job guarantees & big investment in U.S.).

U.S. Steel x Nippon Steel Deal Proposal Blocked (2025 Overview)

Included below are brief details about the proposed purchase of U.S. Steel by Nippon (a Japanese company).

Proposed Transaction

Value: USD $14.9 billion, all-cash offer.

Price per Share: $55.00 per share (around a 40% premium over then-current market price).

Announcement & Approval: Announced in December 2023. Unanimously approved by U.S. Steel’s Board on December 17, 2023.

Key Commitments by Nippon Steel

Standalone Operations: U.S. Steel would continue as an integrated steel company with headquarters in Pittsburgh.

Major Investment: $2.7 billion earmarked for modernizing U.S. Steel’s domestic facilities (e.g., upgrades to aging blast furnaces).

Labor Protections: Agreement to honor existing union contracts and protect workers’ pensions.

Competitive Auction: Nippon Steel won out over domestic and international bidders such as Cleveland-Cliffs, ArcelorMittal, and Nucor.

Why the Deal Was in Negotiation

Financial Struggles

Declining earnings and revenue at U.S. Steel (e.g., net earnings fell from $299 million in Q3 2023 to $119 million in Q3 2024).

High operating costs tied to aging blast furnace infrastructure.

Need for Modernization

U.S. Steel sought capital and technological expertise to shift toward more efficient electric arc furnaces and sustainable steel production.

Nippon Steel’s advanced processes and R&D capabilities were seen as key assets.

Global Competitive Pressures

China’s dominance (producing roughly 60% of global steel) plus strong competitors like ArcelorMittal pressured U.S. Steel to scale up technologically.

Nippon Steel’s potential partnership could significantly enhance competitiveness.

U.S. Steel’s Long-Term Strategy

A sale would inject immediate cash, reduce financial risk, and secure new technology—bolstering U.S. Steel’s market position.

Why U.S. Steel Wanted to Sell to Nippon

Capital Infusion: A $14.9 billion deal plus the promise of $2.7 billion in facility investments.

Technological Upgrades: Nippon Steel’s world-class methods and R&D to modernize U.S. Steel’s blast furnaces and mini-mill capabilities.

Global Reach: Potential synergy to broaden customer bases and possibly collaborate on global supply chains.

Stability for Labor: Nippon pledged to keep union contracts intact, offering reassurance to employees during the transition. Essentially this would’ve enhanced job security for U.S. Steel workers in the U.S. Many U.S. Steel workers wanted the deal to go through (whereas the United Steelworkers Union didn’t… they were at odds).

Major Reasons the U.S. Steel-Nippon Deal Was Blocked

National Security Concerns

Both President Biden and many lawmakers argued a domestically owned steel industry is critical for defense and infrastructure.

Even with Japan being an ally, foreign control was viewed as a potential vulnerability in times of geopolitical crises.

Domestic Industry Protection

Fear that allowing foreign ownership of a major steel producer could erode the U.S. industrial base over time.

Maintaining steel production capacity on U.S. soil was seen as essential for supply chain resilience.

Union & Political Opposition

The United Steelworkers union (USW) strongly opposed the transaction, concerned about future job security, pensions, and bargaining power.

Politicians from both parties echoed these concerns, citing the iconic status of U.S. Steel.

Deadlock at CFIUS

The Committee on Foreign Investment in the U.S. (CFIUS) could not reach a consensus.

This stalemate elevated the final decision to the President, who exercised his authority to block the deal.

Both Trump and Biden Agreed on Blocking

Shared National Security Rationale: Both view a strong domestic steel sector as integral to military readiness and economic strength.

Economic Nationalism: From different political perspectives, each has advocated for “America First” policies when it comes to core industries. Foreign takeovers of iconic U.S. companies can be politically risky.

Union Support: Both administrations have shown solidarity with labor unions (particularly USW), an important constituency in swing states like Pennsylvania, Ohio, and Michigan.

Downsides of Blocking the Deal

Lost Capital Injection: U.S. Steel will not receive the multi-billion-dollar modernization investment that Nippon Steel committed, leaving aging facilities at risk.

Technological Advancement Missed: Nippon’s advanced production methods, R&D, and innovation could have propelled U.S. Steel to be more globally competitive.

Higher Long-Term Costs: U.S. Steel may need to shoulder all modernization expenses itself or seek other, potentially more expensive, financing options.

Foreign Investment Deterrent: Blocking a major acquisition by a close ally (Japan) might discourage future foreign investment in critical U.S. industries.

Strained U.S.-Japan Relations: Japan is a key U.S. partner in the Indo-Pacific region. Blocking this deal could create unease in bilateral economic ties.

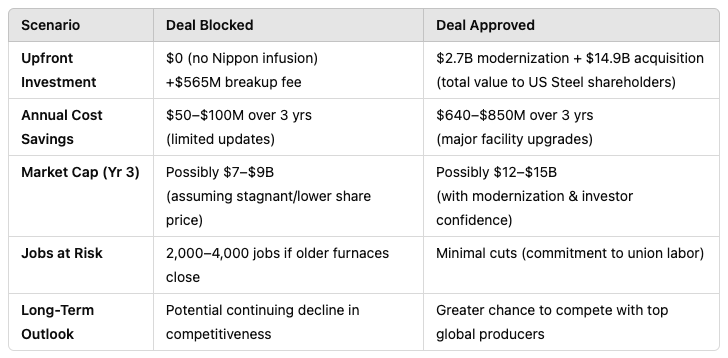

Estimating the Short-Term & Long-Term Impact of Blocking the U.S. Steel-Nippon Steel Deal

Below is a more quantitative, scenario-based analysis of the blocked U.S. Steel–Nippon Steel deal and its potential short- and long-term effects.

While some figures are necessarily approximations, they aim to illustrate the order of magnitude and directional impact of blocking (versus completing) the acquisition.

A.) Short-Term Financial & Operational Impacts

1. Capital Infusion and Modernization

Proposed Nippon Investment: $2.7 billion earmarked for upgrading U.S. Steel’s aging facilities (primarily blast furnaces at Mon Valley, Gary Works, and Granite City).

Immediate Effect of Block:

Foregone Modernization: These investments likely would have occurred over 2–3 years, with an expectation of improving overall cost-efficiency by an estimated 15–20% in those upgraded plants.

Impact on Production Costs: Without modernization, U.S. Steel could spend an incremental $200–$300 million annually (over the next 3 years) to keep its older blast furnaces operating safely and in compliance with environmental regulations.

2. Stock Price and Market Capitalization

Pre-Deal Price: Hovered around $38–$40 per share.

Deal Price: $55 per share, implying a $14.9 billion valuation.

Post-Block Reaction:

Analysts estimate that U.S. Steel’s share price could retreat to the mid-$30s or lower. If it drops from $40 to $32, for instance, that’s a 20% decrease.

In market-cap terms, a drop from $10.8 billion (at $40/share) to $8.6 billion (at $32/share) erases roughly $2.2 billion in shareholder value—significant for a company already carrying notable debt.

3. Breakup Fee

Potential Breakup Fee: $565 million owed by Nippon Steel if the deal definitively fails.

Short-Term Cushion: While $565 million is substantial, it’s far less impactful than the $2.7 billion in direct investment and the broader strategic advantages that would have accompanied a successful acquisition.

Net Effect: The one-time fee partly offsets legal costs or short-term capital needs but does not address long-term modernization demands.

B.) Medium-Term Operational and Competitive Impacts

1. Cost Structure and Profitability

Current U.S. Steel Production Costs: Estimated at $550–$600 per net ton for some blast furnace operations.

With Modernization (Had the Deal Succeeded):

The $2.7 billion could reduce production costs by $40–$50 per ton in 2–3 years.

Over a production volume of ~16–17 million tons/year, that saving could total $640–$850 million annually.

Without the Deal:

U.S. Steel may rely on smaller, incremental capex and high-interest debt, reducing cost savings to perhaps $10–$15 per ton over the next 3–4 years.

Net result is a smaller reduction in the cost structure, making it harder to compete with more modernized producers (e.g., ArcelorMittal, Cleveland-Cliffs, Nucor).

2. Market Share and Capacity

Global Market Context: China and other top producers (e.g., ArcelorMittal) regularly invest billions in modern plants.

U.S. Steel Market Share: Roughly 5–6% of domestic production. Staying competitive requires ongoing large-scale investments, which are now uncertain or more expensive.

Potential Capacity Reductions: If older blast furnaces become too costly to maintain, U.S. Steel might have to idle or shut them, reducing capacity—and with it, domestic steel supply security.

3. Employment and Union Stability

Union Jobs at Stake: Approximately 15,000–20,000 unionized roles in blast-furnace plants.

Deal’s Labor Commitments: Nippon Steel pledged to honor existing contracts and maintain U.S. operations, potentially stabilizing those jobs.

Post-Block Reality:

Without modernization funding, facilities at Mon Valley or Gary Works could face partial shutdown or downsizing within 2–5 years, risking several thousand jobs.

In a worst-case scenario, if outdated assets are retired, you could see a 10–20% workforce reduction—2,000 to 4,000 jobs lost.

C.) Long-Term Strategic and Macroeconomic Considerations

1. National Security and Supply Chain Resilience

Government Justification: Keeping a “strategic” industry like steel under domestic control is a hedge against supply chain disruptions or geopolitical tensions.

Cost of Domestic Ownership: If U.S. Steel under-invests in modernization, reliance on foreign steel in critical periods might ironically increase over time, as U.S. capacity erodes.

Net Impact Over 5–10 Years: The U.S. either has to (1) ramp up federal support/subsidies for U.S. Steel or (2) accept a long-term decline in domestic output.

2. U.S.–Japan Relations and Foreign Direct Investment (FDI)

Japan as a Key Ally: Historically, Japanese investment in the U.S. has been viewed favorably. Blocking such a large deal raises questions about regulatory unpredictability.

Future FDI Impact: Other foreign companies—even from allied nations—may be wary of high-profile acquisitions in strategic U.S. sectors. This can reduce overall FDI by an estimated 5–10% in sensitive industries.

Spillover: Could prompt bilateral tensions, possibly affecting joint ventures in other areas (e.g., semiconductors, automotive, energy).

3. Global Competitiveness and Technological Leadership

Technological Synergy Missed: Nippon Steel invests heavily in high-grade electrical steels, advanced coated steels, and lower-emission processes.

Innovation Gap Risk: Without this technology transfer, U.S. Steel might lag 3–5 years behind leading producers in product innovation and greenhouse-gas reduction strategies.

Environmental Regulations: As carbon emissions rules tighten, plants lacking modernization could face stiff penalties or forced shutdowns, further reducing competitiveness.

Quantifying Potential Net Effects (Long-Term)

Below is a simplified 5-year net-present-value (NPV) style snapshot to illustrate potential outcomes. All figures are broad estimates for demonstration.

Observations:

The blocked scenario might yield a short-term political or strategic “win” on paper but could cost the U.S. steel sector $600M–$850M in annual lost efficiencies within 3–5 years.

Over a 5-year horizon, the total forgone value—when factoring in smaller capital improvements, potential plant closures, and a lower share price—could easily exceed $2–$3 billion in lost enterprise value and operating efficiencies.

Analysis: U.S. Steel Nippon Deal Block: Good or Bad for Long Term?

1. Case for Blocking (Good in the Short Term, but Potentially Costly Later)

Pros

Immediate political capital: Aligns with union interests, avoids foreign control of a “strategic” asset, shores up domestic ownership narratives.

National security posture: Preserves the idea that the U.S. can independently produce crucial steel for defense and infrastructure.

Cons

The lost investment leaves U.S. Steel underfunded for crucial upgrades, raising the risk of capacity closures and job cuts down the road.

Over 5–10 years, failing to modernize effectively could undermine the national security rationale itself if domestic steel capacity erodes anyway.

2. Case for Allowing (Less Politically Popular, Likely Better Economically)

Pros

Injection of $2.7 billion specifically earmarked for modernization could have saved thousands of union jobs long-term and improved competitiveness.

Strengthened ties with a key ally (Japan), setting a favorable precedent for other potential foreign investors from allied nations.

Potentially 2–3% improvement in domestic steel market share by operating more efficiently and capturing new contracts.

Cons

Political risks of perceived “outsourcing” or “foreign takeover,” particularly in an environment focused on economic nationalism.

Some industrial policymakers worry about reliance on any foreign-controlled firm for critical supply chains—even if that foreign partner is an ally.

Quantitative Takeaways

Short-Term Win vs. Long-Term Cost: Blocking the deal yields an immediate political gain and retains nominal domestic ownership. However, the lack of a major capital infusion could impose a $600M–$850M per year efficiency penalty if older plants are not overhauled.

Market Capitalization and Jobs: U.S. Steel’s share price may fall by 20% or more, eroding $2–$3+ billion in market value and potentially jeopardizing thousands of union jobs if the company cannot afford modernization.

National Security Paradox: While blocking preserves “ownership” in name, long-term steel output might still decline without technological upgrades and robust investment—paradoxically weakening actual national security if domestic capacity diminishes.

5-Year Horizon: The net effect is likely negative for U.S. competitiveness unless U.S. Steel finds a comparable investor or secures significant federal and/or private funding. Even then, the cost of capital may be higher, and the modernization timeline longer, than under the Nippon deal.

From a purely economic perspective—and using these rough metrics—the deal’s blockage appears detrimental in the medium to long term (3–7 years), primarily because U.S. Steel is already behind in technological upgrades and environmental compliance.

However, from a short-term political and “domestic control” vantage, blocking might be seen as a win, especially for policymakers who prioritize national security optics and union politics over immediate foreign investment gains.

Bottom Line

Short-Term (0–2 Years): Blocking looks politically favorable; avoids foreign takeover optics, appeases unions.

Medium-Term (3–5 Years): Risk of underinvestment, higher production costs, and eroding competitiveness.

Long-Term (5+ Years): If no alternative capital emerges, potential declines in domestic steel production could undermine the very national security and job-protection goals that motivated the deal’s blockage in the first place.

My Main Criticisms of the U.S. Steel-Nippon Deal Blockade…

The U.S. government stepping in to prevent a U.S. company from completing a deal with a company from a foreign ally was stupid (in my opinion). If anything shady ever went on with Nippon we could easily seize control of the plants in the U.S. anyway.

By blocking this deal, it may signal to foreign allies that they should be more cautious about trying to do deals and/or invest in the U.S. and it may ironically reduce job security for U.S. Steel workers, increase inflation, and decrease U.S. steel production (difficult to keep up with technology and efficiency) – which could lead to the result that the U.S. is trying to avoid (long-term).

1. Government Overreach

Excessive Intervention: The U.S. government, by outright blocking the deal, exerts direct control over private-sector M&A decisions.

Undermines Shareholder Rights: Shareholders of U.S. Steel unanimously approved the deal, yet this democratic corporate process was overridden by federal authorities.

Risk of Politicization: Such an intervention can set a precedent where political agendas or optics drive major decisions, rather than economic or market-based considerations.

2. Anti–Free Market

Restricts Competition: Preventing foreign acquisitions of U.S. firms can limit the free flow of capital.

Stifles Efficiency: In a truly free market, underperforming companies can be acquired or restructured by those with the resources and expertise to improve them—in this case, Nippon Steel’s infusion of technology and funds.

Market-Distorting Signals: Sends a message that certain industries are off-limits to global competition, which can deter other potential investors (even from allied nations).

3. Inflationary Pressures

Tariffs and Subsidies: With the deal blocked, the U.S. government is more likely to expand protective tariffs or introduce new subsidies to keep U.S. Steel afloat.

Higher Prices: Tariffs raise input costs for downstream manufacturers (like automakers or construction firms), who pass those costs on to consumers.

Public Spending: If direct subsidies or bailouts become necessary, it increases federal spending, potentially fueling inflation further.

4. U.S. Steel Becomes Less Competitive

Missed Capital Investment: The $2.7 billion modernization plan promised by Nippon Steel won’t materialize. U.S. Steel’s outdated facilities remain a drag on productivity.

Lost Technology Transfer: Nippon’s advanced steelmaking technology could have improved U.S. Steel’s operational efficiency and environmental performance—both are now lost opportunities.

Worsening Global Position: Competitors (e.g., Nucor, ArcelorMittal, and Chinese state-backed firms) continue to invest heavily, leaving U.S. Steel further behind.

5. Less Job Security (Ironically)

Downsizing Likely: Without the deal’s promised capital infusion, U.S. Steel may be forced to close older furnaces or lay off workers to cut costs.

Contractual Guarantees Lost: The merger agreement included honoring union contracts and pensions, which could have safeguarded positions more effectively.

Financial Instability: A less profitable, less modernized U.S. Steel is more prone to cyclical downturns, heightening employment risks.

6. Higher Steel Costs Domestically

Lack of Foreign Investment: In a competitive market, foreign investment can drive down costs by introducing new efficiencies. Blocking these investments tends to keep prices higher.

Tariff-Driven Pricing: If the U.S. government maintains or increases tariffs in lieu of modernization, domestic steel prices will remain inflated for consumers and downstream industries.

Reduced Innovation: Without international best practices and cutting-edge R&D, there’s less incentive for cost-reducing technological breakthroughs.

7. Company from an Allied Nation

Japan Is a Key U.S. Ally: Unlike acquisitions from adversarial states, a Japanese investment poses far less geopolitical risk.

Friend-Shoring Opportunity: The U.S. strategy of “friend-shoring” or “ally-shoring” is meant to shift critical supply chains to trusted partners—blocking this deal contradicts that concept.

Diplomatic Fallout: This decision could strain U.S.-Japan economic ties, discouraging future investments from a reliable partner that shares strategic interests in the Indo-Pacific. (It probably won’t but it’s not a good look.)

8. Contradiction in Policy Goals (Optional Additional Point)

National Security vs. Economic Viability: The stated reason for blocking the deal is national security and preserving domestic steelmaking. Ironically, without fresh capital, U.S. steel capacity might shrink over time, weakening the very sector the government aims to protect.

Environmental and Technological Lag: Investing in modern, cleaner steel technology is also a security matter in the broader sense (energy independence, emissions standards). Blocking an ally’s investment can slow America’s advancement on these fronts.

How can the U.S. turn the blocked Nippon deal into a win for domestic steel production?

I think it was probably dumb to block the U.S. Steel x Nippon deal, but understand the rationale.

Blocking this deal may hurt both U.S. steel workers and U.S. steel production long-term (without government strategy & intervention)… this would be the opposite of what the U.S. is trying to achieve.

Anyways, we knew that since neither Biden, Trump, nor the United Steelworkers Union wanted this deal to happen - it likely didn’t stand a chance.

The question then becomes: How does the U.S. turn things around to truly “Make Domestic Steel Production Great Again”?

Theoretically the U.S. can still turn this into a win if they come up with and execute a highly-strategic plan to increase the competitiveness (cost-efficiency) of domestic (made in USA) steel production.

If they fail to strategize and/or execute - blocking this deal will look like a misguided and foolish populist decision that was erroneously perceived as putting “America First” (but ended up putting “America Last”).

Here is a general framework I came up with for making American steel globally competitive and/or dominant within 5-10 years.

PHASE 1 (0–18 Months): “Shock and Awe” for Rapid Competitiveness

1. Extreme “Buy U.S. Steel” Infrastructure Mandates

Federal Infrastructure Bill (e.g., $1–$1.5 trillion) with 100% U.S. steel requirement for roads, bridges, public buildings, and defense contracts.

State-Level Incentives: States receive higher federal matching funds only if they use American steel.

Immediate Rollout: Fast-track procurement so steel orders hit the market within 6 months.

Why This Works Short-Term

Stimulates Demand: Could boost domestic steel usage by 5–10+ million tons per year, pushing capacity utilization above 90% almost overnight.

Price Stability: Mills can run near full capacity, dropping per-ton overhead costs quickly.

2. Rapid Permitting & Regulatory Rollback

One-Stop Permitting: Combine environmental and construction permits into a single expedited office.

Temporary Waivers: Grant 2–3 year waivers on non-critical compliance for mills expanding capacity or refurbishing.

24/7 Construction Approvals: States/federal agencies allow around-the-clock construction to finish expansions in record time.

Why This Works Short-Term

Cuts Time to Market: Expansion/modernization projects can complete in 12 months instead of 2–3 years.

Cost Savings: Fewer compliance hurdles = immediate start on new lines or EAF conversions.

3. Aggressive Tariffs & Anti-Dumping with Real-Time Enforcement

Automatic Tariff Triggers: If a foreign producer’s landed cost is more than 15% lower than U.S. production cost, immediate tariffs are imposed.

Real-Time Monitoring: Use advanced data analytics at Customs to detect and act on import surges or suspiciously low pricing.

Refine Section 232: Keep strong national-security-based measures to prevent import floods, but update them as U.S. mills hit cost goals.

Why This Works Short-Term

Instant Market Protection: Prevents cheap steel from crushing domestic prices.

Ensures Profit Margins: Domestic mills can reinvest revenue in modernization instead of losing market share to underpriced imports.

4. Major Capital Infusions for Immediate Cost Cutting

Zero-Interest Loans / Rapid Grants: $5–$10 billion in direct federal capital for EAF conversions and critical upgrades to existing blast furnaces (if it’s faster).

Accelerated Depreciation: 100% write-off in Year 1 for new machinery, robotics, and process control systems.

Minimal Red Tape: Simple eligibility—show you’re adding capacity or slashing costs, and you get funded.

Why This Works Short-Term

Drops Production Costs by $20–$50/ton: Upgraded equipment, better energy efficiency, reduced downtime.

Fast Payback: Extra liquidity helps mills start modernization now, not in 2–3 years.

5. Supercharged Energy Cost Reductions

Discount Energy Zones: Lock in sub-market electricity/gas rates for 5+ years around steel hubs (Great Lakes, Gulf Coast).

Pipeline/Utility Fast-Track: Expand natural gas pipelines to deliver consistent, cheap feedstock.

Federal Tax Breaks for Utilities: If they offer below-market industrial power rates to steel mills that increase capacity by at least 10–20%.

Why This Works Short-Term

Energy Is 15–25% of Cost: Cutting $10–$20/ton is huge for competitiveness.

Immediate Action: Government can broker deals with utilities in under 12 months if done aggressively.

PHASE 2 (18+ Months Onward): Ensuring Long-Term Global Dominance

6. Full-Scale Transition to Modern EAFs + Advanced Technologies

EAF Conversion Blitz: By Year 3–5, aim to replace or supplement all major blast furnaces with EAF capacity—funded partly by the Phase 1 revenue surge.

AI/Automation Mandate: Require new or upgraded lines to incorporate real-time process control (machine learning) and robotics for minimal labor overhead.

Strategic Upgrades: Integrate next-generation furnace technologies (e.g., near-net-shape casting) to reduce finishing steps and costs.

Why This Works Long-Term

Lower Operating Costs: EAFs often operate $30–$50/ton cheaper than legacy blast furnaces, especially with cheap scrap or direct-reduced iron (DRI).

Flexible Production: Easier to switch between product types and market demands—staying competitive globally.

7. Advanced R&D and High-Value Steel Specialization

National Steel R&D Consortium: Fund a consortium (via DOE, DoD, etc.) dedicated to advanced alloys (e.g., high-strength automotive steels, grain-oriented electrical steel).

Rapid Prototyping & Scale-Up: Provide testing facilities and pilot lines so breakthroughs can hit commercial scale within months, not years.

Patent & IP Acceleration: Fast-track intellectual property filings to ensure U.S. producers get first-to-market advantage on new steel grades.

Why This Works Long-Term

High-Margin Products: Specialty steels can command premium prices, partially offsetting higher U.S. labor costs.

Global Tech Leadership: If the U.S. leads in advanced steel, it can export both commodity and premium products, dominating multiple market segments.

8. Optimized Raw Material Supply and Logistics

Domestic Scrap Optimization: Set national scrap collection standards, ensure high-quality sorting, possibly restrict scrap exports so EAFs have ample cheap feedstock.

DR-Grade Iron Ore: Fast-track mining and production of direct-reduced (DR) pellets (especially in Minnesota’s Iron Range) for EAF usage.

Alloy Metals Security: Secure partnerships or stockpiles with allied nations (e.g., Canada, Australia) for critical alloys (nickel, chromium, manganese) to avoid supply disruptions.

Why This Works Long-Term

Stable Input Costs: Minimizes reliance on volatile global raw material markets.

Security: Prevents supply shocks that could undercut cost or capacity expansions.

9. (Optional) Tactical Upskilling for High-Tech Mills

Short, Targeted Training: Although we’re avoiding “fluff,” certain advanced robotics and AI systems do require specialized operators and technicians.

Production-Focused: Pair training with immediate lines going live, so new skills directly reduce downtime, boost throughput.

Automation First: Keep it lean—focus on cross-training a small cadre who can run multiple stations, maximizing labor efficiency.

Why This Is Important Long-Term

Supports Ultra-High-Tech Operations: You can’t run advanced lines without at least a handful of skilled technicians.

Minimal Overhead: Focus only on the operationally critical skills, not broad workforce programs.

PROJECTED TIMELINE & OUTCOMES

Phase 1 (First 6–18 Months)

Demand & Protection: Domestic capacity utilization spikes from ~75–80% to 90–100% within 6–12 months due to mandated infrastructure projects and aggressive tariffs.

Cost Reduction: Immediate modernization, cheap energy deals, and easier permitting could knock $20–$50/ton off many mills’ operating costs.

Rapid Expansion: Up to 5–10+ million tons of new annual demand is met by existing mills running near capacity or quickly expanding.

Phase 2 (Year 2–5)

Mass EAF Adoption: Significant portion of older blast furnaces converted or supplemented by EAF lines. Expect a $30–$50/ton production cost advantage over legacy setups.

Tech Leadership: With strong R&D backing, U.S. mills produce premium steels at scale, capturing higher-margin global segments (auto, EV motors, infrastructure requiring ultra-strong steels).

Global Exports & Dominance: Protected by stable raw materials, cutting-edge processes, and strong brand credibility, U.S. steel gains share in both commodity and specialty markets.

BOTTOM LINE

Short-Term: Use a “shock and awe” approach—massive government-backed demand, immediate protective tariffs, deep regulatory rollbacks, and quick capital injections. This surges domestic production, crushes cheap imports, and ensures near-instant profitability for U.S. mills.

Long-Term: Channel those short-term profits into full-scale EAF conversions, advanced automation, R&D-driven specialty steels, and stable raw material supply chains. Over 2–5 years, this positions the U.S. as both the low-cost and high-tech leader, capable of dominating global steel markets sustainably.

By merging these two phases, America gets the rapid competitiveness boost and the structural upgrades needed for global steel leadership—without over-focusing on “woke” elements or ignoring the critical role of advanced technology in securing the future.

U.S. Steel & Domestic Steel Production Under Trump (2025-2030)

It is likely that Trump will impose moderate tariffs and massive deregulation, which should make U.S. Steel and domestic steel production more cost-effective and competitive on a global scale.

Odds of Each Scenario

Scenario A (Moderate Tariffs & Deregulation): ~50%

Scenario B (High-Intensity “Shock and Awe”): ~20%

Scenario C (Incremental / Status Quo-ish): ~30%

Competitiveness by 2030

Scenario A: Likely improvement over current baseline. Domestic utilization around 85–90%. Per-ton costs drop slightly, but U.S. Steel may still trail global leaders (like advanced Chinese or mini-mill producers) unless it aggressively invests in EAFs.

Scenario B: Potentially transformative if fully realized: U.S. Steel could approach top-tier cost efficiency if billions in new capital and mandates roll out quickly. The risk is political feasibility.

Scenario C: Minimal net change versus today. Some short-term stability from moderate tariffs, but no major modernization wave.

Contrast with Nippon Deal

Nippon: Faster modernization, direct technology infusion, long-term competitiveness gains. But ownership partially goes overseas, which was the primary concern of U.S. policymakers and labor unions.

Trump-Style Approach: Relies on tariff-driven revenue and government incentives to finance upgrades. More domestic “control,” but modernization timetables are uncertain and can be undermined by political and legal headwinds.

In Sum: A second Trump term will probably make U.S. Steel more competitive in the domestic market through higher tariffs, “Buy American” rules, and moderate deregulation, but full global leadership is less certain and may hinge on either (a) an ambitious “shock and awe” package—less likely politically—or (b) extraordinary corporate reinvestment efforts that replicate what Nippon’s direct capital might have achieved more swiftly.