LiDAR in 2025: The Gold Standard for Level 4 Autonomous Vehicles (AVs) - Cost-Performance Evolution, Safety, Future of FSD

Elon Musk has long criticized LiDAR, but it gets more cost-effective each year... and has worked well for Waymo and Baidu

Autonomous vehicles (AVs) promise transformative benefits in safety, mobility, and efficiency. The sensors enabling real-time environmental perception remain a pivotal debate—particularly LiDAR (Light Detection and Ranging), which many Full Self-Driving (FSD) developers deem essential.

Waymo, Baidu, and Mobileye maintain that LiDAR is central to reliable, geofenced autonomy.

Tesla initially pivoted to a “vision-only” approach but recently reintroduced high-definition radar in Hardware 4 (HW4) vehicles due to the lack of progress with “vision-only.” Tesla still rejects LiDAR.

State of the Industry (as of 2025)

Waymo operates driverless robotaxi services in Phoenix/SF using LiDAR-based sensor fusion.

Baidu Apollo deploys multi-LiDAR fleets in major Chinese cities.

GM Cruise ended its SF-based program, once a LiDAR-focused solution, due to funding and regulatory/incident issues.

Tesla has begun installing a new high-definition radar (“Phoenix”) in Model S/X with HW4 hardware, supplementing cameras for better object detection in bad weather. Nevertheless, Tesla explicitly continues to NOT adopt LiDAR, citing cost and Elon Musk’s belief that neural networks + cameras are mostly sufficient with added radar at scale.

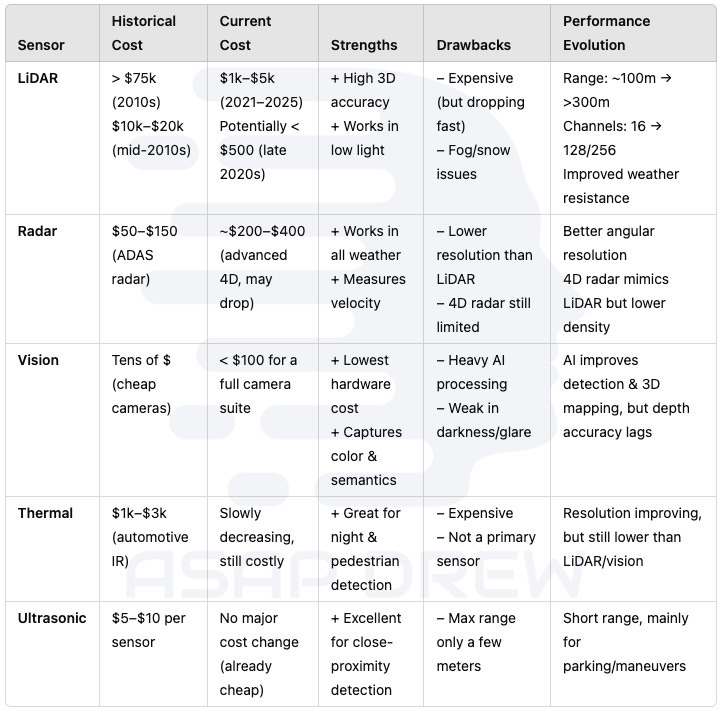

Sensing Modalities for Autonomous Vehicles (AVs) 2025

LiDAR, Cameras (Vision), Radar, Thermal (Infrared), Ultrasonic

All are used in some combination by different AV companies. The table below highlights cost-efficiency and performance evolution over time.

Cost-Efficiency & Performance Evolution

Observations:

LiDAR remains the highest-accuracy sensor for 3D range info, with drastically dropping costs.

Radar is excellent in inclement weather and for velocity detection, now returning to Tesla’s sensor suite in certain models.

Cameras remain the cheapest, but purely vision-based autonomy (i.e., no LiDAR, no radar) has shown persistent edge-case issues.

The Evolution of LiDAR (2010-Present): Cost-Performance Analysis

Early 2010s: Expensive, Bulky, and Low-Resolution

LiDAR systems relied on mechanical spinning units, costing $75k–$100k with a range of ~100m and 16 channels.

Radar was basic, and cameras were primarily used for lane-keeping.

Mid-2010s: Emergence of Solid-State LiDAR

Costs dropped to $10k–$20k as solid-state technologies (MEMS, Flash) began to emerge.

Channel counts increased to 32–64, and radar evolved into short/long-range combinations.

2020s: Automotive-Grade LiDAR Becomes Feasible

By 2021–2025, LiDAR reached $1k–$5k at moderate volumes, with 128–256 channels and ~300m range.

Resolution improved from 16 beams → 128/256 beams, creating denser point clouds.

Weather hardening: Advanced signal processing and coatings helped reduce rain/snow interference.

2026–2030: LiDAR Gets Cheaper, More Robust, and Smarter

LiDAR costs could fall to $300–$500, improving performance in adverse weather.

FMCW LiDAR (Frequency-Modulated Continuous Wave) introduces Doppler velocity measurement, boosting reliability in challenging conditions.

Radar becomes a widely used secondary sensor, while vision remains universal for color classification.

2030+: Sensor Fusion, Mass Production, and High Precision

If mass production scales, LiDAR could drop to $200–$300.

Many L4 autonomous vehicles will adopt sensor fusion (LiDAR + cameras + radar) for redundancy.

Vision-only may persist in niche applications unless a major AI breakthrough significantly enhances perception reliability.

Range expansion: Some top-tier LiDAR systems may exceed 300m, becoming vital for highway autonomy.

Analysis: Continuous improvements make LiDAR more capable and affordable, driving adoption among major AV programs for robust, high-level autonomy.

Other Sensor Competitors & Progress

Advanced Radar & Its Progress

Standard Radar: Good at detecting moving objects, limited resolution for object shape.

Imaging & 4D Radar: Adds vertical dimension for partial 3D data. Better in adverse weather, but not as detailed as LiDAR.

Vision-Only Advances & Gaps

Pros: Extremely cheap, no extra hardware beyond cameras.

Cons: Complex AI for depth, illusions, glare, edge cases. Regulators remain cautious about single-sensor autonomy.

Tesla: After removing radar entirely in 2021, has now recognized certain limitations, bringing back a 4D radar in HW4 for select models.

Other Sensors (Thermal, Ultrasonic)

Thermal: Niche for nighttime/pedestrian detection but costly, rarely used as primary.

Ultrasonic: Standard for short-range tasks (parking), inadequate for mid-/high-speed AV.

LiDAR Manufacturers (2025)

Waymo: Manufactures its own LiDAR sensors (began this in 2012 after initially licensing from Velodyne).

Velodyne: Classic spinning LiDAR pioneer, merging with smaller players.

Luminar: Partnerships with Volvo, Mercedes; aims for $500–$1,000 automotive LiDAR.

Innoviz: Supplies BMW, VW. Known for solid-state reliability.

Hesai, RoboSense (China): Large-scale production for Baidu, Xpeng.

Ouster, Aeva: Pushing FMCW LiDAR, measuring Doppler velocity.

Key Differentiators:

Cost: Below $1k in OEM-scale volumes.

Resolution & Range: 128–256 channels at 200–300m+ is the new standard.

Automotive Certification: Ruggedized designs, meeting safety/regulatory demands.

OEM Contracts: Partnerships with major automakers and AV programs.

Major AV Companies Embracing LiDAR

1. Waymo (Alphabet)

Approach: Multi-sensor fusion (LiDAR, cameras, radar).

Geofenced Robotaxi: Fully driverless in Phoenix, expanding in SF.

Safety Metrics: High miles/disengagement, ~85%+ reduction in collisions vs. human drivers in certain zones.

2. Baidu Apollo (China)

LiDAR-Heavy: At least 2–4 LiDAR units per vehicle, plus cameras/radar.

Apollo RT6: ~$37k total cost, showing LiDAR can be integrated affordably at scale.

Deployment: Supported by Chinese government in major cities.

3. Mobileye (Intel)

Camera-based ADAS for L2 in many cars.

L4: “True Redundancy” demands LiDAR, radar, cameras.

Partnerships: With Innoviz, Luminar, etc. for LiDAR modules.

Major AV Companies Rejecting LiDAR

1. Tesla

Historical Stance: After 2021, Tesla removed radar and ultrasonic sensors, proclaiming “vision-only” was sufficient.

HW4 & Radar Return:

Mid-2023 teardowns of Model S/X with HW4 revealed a high-definition “Phoenix” radar module operating at 76–77 GHz.

Radar is meant to handle poor weather and reduce phantom braking, bridging performance gaps.

Not universal: Some Model Y HW4 units ship without radar, likely for cost or supply reasons, but higher-end models are testing it.

Still No LiDAR: Elon Musk dismisses LiDAR for its cost and complexity, maintaining that cameras plus advanced AI—and now a refined radar—can suffice for FSD.

Why the Partial Reversal?:

Phantom Braking & Crash Reports: Vision-only faced difficulties with stationary objects.

Improved Tech: This new radar is higher fidelity than older modules, aiming to complement cameras without returning to the old “noisy” radar approach.

Takeaway: While Tesla remains officially anti-LiDAR, the reintroduction of radar in HW4 underscores the limitations of pure vision. Tesla’s final stance is now more of a “camera + advanced radar” approach, but still no LiDAR.

2. Xpeng

Initial Use: Dual LiDAR in P5 (2021) for city driving.

Subsequent Pivot: Some newer Xpeng models omitted LiDAR, citing cost; tries advanced radar + camera combos.

LiDAR: Safety & Reliability Assessment

Disengagement Rates & Crash Data

Waymo, Baidu (LiDAR-based):

Tens of thousands of miles between disengagements.

Demonstrated fewer collisions than human drivers in controlled environments.

GM Cruise (LiDAR-based):

Initially low disengagement rates in San Francisco.

Suspended operations after a pedestrian incident and financial difficulties.

Tesla (Vision + Radar, No LiDAR):

No official Level 4 testing; FSD Beta remains Level 2 (L2).

Frequent user-reported interventions in complex urban scenarios.

Phantom braking issues (post-2021) were partially addressed with new HW4 radar.

Is LiDAR Safer Compared to Other Technologies?

Direct Depth Sensing: LiDAR’s 3D mapping prevents perceptual errors common in camera-only systems. Reduces the risk of false positives and negatives from visual illusions.

Level 4 (L4) Autonomy: Every operational "no-safety-driver" fleet relies on LiDAR. No known L4 system relies solely on vision or radar.

Tesla’s Radar Reintroduction: Marks a shift back toward sensor redundancy but still lacks LiDAR.

Scaling & Handling Edge Cases

Construction Zones & Unusual Obstacles: LiDAR’s precise geometry scanning improves detection of temporary barriers and objects.

Weather Challenges: Snow and fog degrade LiDAR, vision, and radar to some extent. Most AVs restrict operations under extreme weather conditions.

Assessment: LiDAR remains the Gold Standard for Level 4 Autonomy due to its direct depth perception, superior object recognition, and proven safety record in controlled settings. However, cost, scaling challenges, and weather limitations continue to influence the debate on sensor strategy.

LiDAR’s Future Outlook vs. Alternatives

Advanced Radar / 4D Radar

Could eventually approach LiDAR’s resolution in simpler conditions, but so far not achieving LiDAR-level detail in complex shapes.

Vision + AI Revolution

If AI overcame all edge cases, LiDAR might become optional. Tesla and Xpeng see this as a future possibility, but real-world data still favors multiple sensors.

FMCW LiDAR

An evolution of LiDAR adding Doppler velocity; potentially more robust in inclement weather. Not a separate sensor category—still “LiDAR-based.”

Odds of LiDAR Being Overtaken?

Short Term (5–7 years): Low. Most proven L4 systems rely on LiDAR.

Long Term (beyond 2032): Maybe a ~20–30% chance that a breakthrough in radar or AI vision reduces LiDAR’s necessity. But sensor fusion likely remains the mainstream approach.

Investment Alpha in LiDAR Suppliers or LiDAR-Centric AV Companies?

The way I think about this is there’s a lot of competition in the LiDAR supplier sector with a few dominant names.

Perhaps there’s some near-term alpha in certain companies if you really dig-in, but I’d be hesitant because picking a specific winner is difficult and the longevity of LiDAR remains unknown.

The best way to capitalize on LiDAR is to focus on companies leveraging LiDAR for their full-self-driving (FSD) programs.

Why? If LiDAR becomes outdated or obsolete, they’ll pivot to whatever is best — and you’ll still have a healthy investment.

You also don’t know how many total companies will order LiDAR… so TAM may be limited. Waymo seems like a solid play because they benefit from making their own in-house LiDAR and have fleets of AVs they can retool if LiDAR becomes obsolete.

LiDAR Suppliers

Rationale: As LiDAR integrates into mainstream automakers (for future L3/L4 ADAS) and robotaxi fleets, suppliers with major production contracts can see revenue scale quickly.

Key Considerations: Look for firms with OEM partnerships. Watch for signs of stable, high-volume deals that lock in revenue beyond prototypes.

AV Platform Companies Using LiDAR

Waymo is under Alphabet (GOOGL); Baidu (BIDU) runs Apollo. Both emphasize LiDAR-heavy strategies for driverless fleets.

Rationale: If LiDAR-based robotaxis continue to be first to market with safe driverless operations, these parent companies’ AV divisions could deliver new revenue streams or cost savings (no human drivers).

Considerations: Both operate large-scale, real-world LiDAR fleets. Progress in more cities and positive safety data can boost investor confidence in each tech giant’s AV arm.

Final Take: LiDAR Evolution for AVs (2025)

LiDAR has evolved from a prohibitively expensive research tool ($75k–$100k) to a sub-$5k—and soon possibly sub-$500—solution with dramatically improved range (300m+), resolution (128–256 beams), and weather hardening.

Despite Tesla’s original pivot to pure vision, Hardware 4 reintroduces a refined HD radar to address phantom braking and poor-weather vulnerabilities. Yet, Tesla still eschews LiDAR on cost grounds.

Meanwhile, Waymo, Baidu, and other successful driverless programs leverage LiDAR-based sensor fusion for geofenced Level 4 operations, achieving real-world driverless service.

Investment in LiDAR suppliers (Luminar, Innoviz, Hesai, etc.) and sensor-fusion AV developers (Waymo, Mobileye, Baidu) remains robust. Regulators and public often trust multi-sensor setups more, especially after incidents like GM Cruise’s abrupt shutdown following a pedestrian crash.

Looking ahead, if LiDAR costs continue to plummet and reliability continues rising, it will likely stay central for autonomous vehicles—particularly for driverless (Level 4–5) operations—well into the 2030s.

While advanced radar or a radical AI vision leap might reduce LiDAR’s importance eventually, current trends firmly position LiDAR as the go-to high-resolution sensor for the safe, reliable rollout of automated driving.

References:

Anderson, J. M., Kalra, N., Stanley, K. D., Sorensen, P., Samaras, C., & Oluwatola, O. A. (2014). Autonomous Vehicle Technology: A Guide for Policymakers. RAND Corporation.

SAE International. (2022). The Role of LiDAR in Autonomous Driving: Challenges and Opportunities.

Tesla Inc. (2021–2022). Investor Communications and FSD Beta Release Notes.

Luminar Technologies. (2022). Advances in LiDAR: Cost Reduction and Performance Enhancements.

Deloitte Insights. (2022). Sensor Technologies in Autonomous Vehicles: A Comparative Analysis.

Waymo. (2023). Waymo Safety Report.

McKinsey & Company. (2023). Autonomous Vehicles: Investment and Technology Outlook.

California DMV. (2022–2023). Autonomous Vehicle Disengagement Data Reports.

Cruise. (2023). Company Information.

Baidu Apollo. (n.d.). Company Information.

Tesla Quarterly Safety Reports. (2022–2023). Company Reports.

Mobileye (Intel). (2022). Annual Report: Sensor Integration and Redundancy in Advanced Driver Assistance Systems.

Innoviz Technologies. (2023). Scaling Solid-State LiDAR for Automotive Applications.

Industry Analyst Report. (2023). Comparative Study: LiDAR, 4D Radar, and Vision-Only Systems.

Hesai Technology. (n.d.). Company Information; Velodyne. (n.d.). Company Information.