Asteroid Mining in 2026: Who is Closest?

Which company will be first to mine an asteroid? And will they target metals or... water?

In tech circles, “asteroid mining” has been pitched for more than a decade as a civilization-level moonshot. I wanted to see what’s real in 2026.

Who is flying hardware? What are they targeting? And does any version of the biz have a credible ROI path?

In early 2026, nobody has commercially mined an asteroid; no company has extracted, processed, and delivered sellable material from space at meaningful scale.

The reason is fairly simple: “asteroid mining” is two different businesses with totally different difficulty and economics:

Earth-return precious metals (PGMs): return high-value metal to Earth via reentry capsules. Engineering is brutal, and commodity markets fight you.

In-space water/volatiles: extract water and sell it in space (propellant, life support, shielding). Economics are cleaner because the benchmark is avoided launch/transport cost, not terrestrial mining.

TL;DR: If asteroid mining ever becomes a real business, it likely starts with water/volatiles sold in space, not platinum returned to Earth.

What Materials Are We Talking About?

Asteroids are not all the same.

Composition varies enormously, and the target material depends entirely on which business model a company is pursuing.

The popular press tends to say “platinum” as shorthand, but the actual commercial pitch is almost always about platinum-group metals (PGMs) as a basket, not just platinum alone.

And the most plausible early resource isn’t a metal at all.

1. PGMs (Earth-return value density)

Product: PGMs (Pt/Pd/Rh/Ru/Ir/Os)

Customer: Earth commodity buyers

Why it can work: extreme value density per kilogram

Main failure mode: refining + return reliability + market depth constraints

This is the “metallic asteroid” thesis. The target is the six platinum-group metals: platinum, palladium, rhodium, ruthenium, iridium, and osmium. These are the metals with enough value per kilogram to potentially justify the cost of a deep-space round trip.

AstroForge repeatedly frames its goal as extracting platinum-group metals, not just platinum. Their Vestri mission press materials describe the objective as evaluating asteroids for PGMs including platinum, palladium, rhodium, and iridium.

Their Odin mission debrief “Odidn’t” describes the goal as validating whether the target asteroid is “rich in platinum group metals.”

So no, it’s not “only platinum.” Platinum is just the headline metal people recognize. The target basket is all six PGMs.

2. Water / volatiles (in-space fuel and propellant)

Product: water / volatiles

Customer: depots, tugs, cislunar operations

Why it can work: priced against avoided launch + transport cost

Main failure mode: the market might not exist yet (no depots, no cadence)

This is the “don’t return commodities to Earth; sell in space” thesis.

The target is water, which can be used directly for life support and radiation shielding, or decomposed into hydrogen and oxygen for rocket propellant.

Karman+ describes missions to mine regolith material and extract water for refueling in orbit

Optical mining approaches (TransAstra/NASA NIAC lineage) are explicitly about extracting water and other volatiles from carbonaceous material using concentrated sunlight inside contained processing bags

Don’t asteroids contain many metals? (Gold, Cobalt, Nickel, Tungsten, etc.)

They can, but contents vary by asteroid.

Top targets (the only ones anyone is seriously pursuing):

Water (H₂O): The best early target, full stop. Worthless on Earth, enormously expensive to launch to orbit. Potentially simpler to extract from C-type asteroids than metals (if thermal/microwave extraction works reliably in microgravity). Value comes entirely from avoided launch cost. This is what Karman+ and TransAstra are building toward.

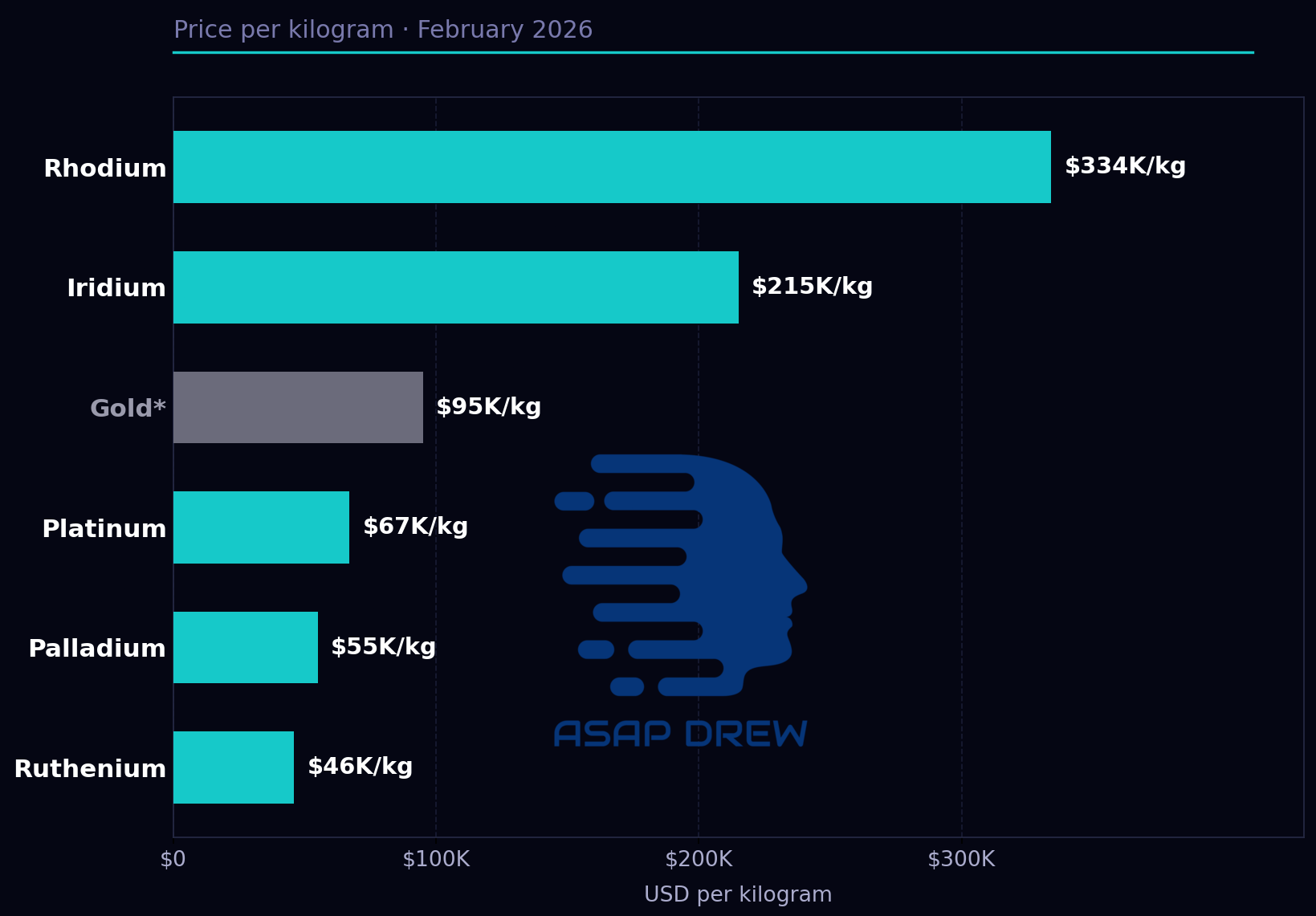

Rhodium (Rh): ~$334K/kg (~$10,400/oz as of Feb 2026). The most valuable PGM by far. Extremely rare on Earth, tiny market, but extraordinary value density per kilogram.

Iridium (Ir): ~$215K/kg (~$6,700/oz). Crucibles, spark plugs, electronics. Very dense, very rare.

Platinum (Pt): ~$67K/kg (~$2,075/oz). Catalysts, electronics, fuel cells. The headline metal in AstroForge’s pitch.

Palladium (Pd): ~$55K/kg (~$1,739/oz). Autocatalysts, electronics, hydrogen purification. Similar Earth-return case to platinum.

Ruthenium (Ru): ~$46K/kg (~$1,430/oz). Electronics, catalysts. Lower profile but still significant value density.

Osmium (Os): No clean industrial spot market comparable to the other PGMs. Specialty pricing exists for crystalline products, but it’s not traded like platinum or palladium. Would come along for the ride with other PGM extraction, not targeted independently.

Marginal (probably not worth the trip on its own):

Gold (Au): ~$95K/kg sounds great, but Earth’s gold supply is enormous (~3,600 tonnes mined per year). Asteroid gold would be a rounding error. It might show up as a byproduct of PGM extraction, but nobody is designing a mission around gold.

Impractical for Earth return (value density way too low):

Iron (Fe): ~$0.75/kg on Earth. Could be useful for in-space construction someday, but that requires a large orbital industrial base that doesn’t exist.

Nickel (Ni): ~$16/kg. Same story as iron. Only useful as structural feedstock in orbit.

Cobalt (Co): ~$33/kg. Battery and superalloy demand exists on Earth, but value per kg is far too low to justify a deep-space round trip.

Tungsten (W): ~$35/kg. Refractory uses, but not remotely worth a space mission.

These low-value metals are what make up the bulk of asteroid mass. They’re why headlines say “this asteroid is worth $10 trillion.”

But you’d never design a mission to return iron or nickel to Earth. If they ever matter commercially, it’ll be as raw feedstock for building things in orbit, decades from now.

Reality on materials:

Metals realistically targeted: PGMs as a group (Pt/Pd/Rh/Ru/Ir/Os), not “platinum only.”

Most plausible early resource: Water/volatiles for in-space use, not metals to Earth.

Everything else (iron, nickel, cobalt, etc.): Only make sense for in-space construction once a large orbital industrial base exists, which is decades away at minimum.

Asteroid Types

Three asteroid classes matter for mining:

C-type (carbonaceous): The most common (~75% of known asteroids). Rich in water, bound up in hydrated clay minerals. Also contain organic compounds, carbon, and some phosphorus. These are the targets for water/propellant extraction.

S-type (stony/silicaceous): Contain significant metal fractions, mostly iron, nickel, and cobalt, with trace amounts of precious metals. According to NASA, a small 10-meter S-type asteroid contains about 650,000 kg of metal, including roughly 50 kg of rare metals like platinum and gold.

M-type (metallic): Rare but contain up to 10x more metal than S-types. Essentially chunks of planetary cores, dominated by iron-nickel alloy with commercially significant concentrations of PGMs.

Platinum-rich asteroids may contain grades of up to 100 grams per ton, which is 10-20x higher than open-pit platinum mines in South Africa.

A single 500-meter platinum-rich asteroid could theoretically contain nearly 175 times the annual global platinum output.

But “contains” and “can profitably extract and deliver” are very different statements.

Asteroid Mining Companies in 2026

1. AstroForge

Target: Platinum-group metals (platinum, palladium, rhodium, iridium) from metallic near-Earth asteroids

Founded: January 2022 by Matthew Gialich (CEO) and Jose Acain (CTO), in Huntington Beach, California

Team size: ~35-42 employees as of 2025

Total funding: $55-56M across 4 rounds

Key investors: Nova Threshold (led Series A), Seven Seven Six (Alexis Ohanian’s fund), Initialized Capital, Y Combinator, Caladan Capital, Uncorrelated Ventures, plus angel investor Jed McCaleb (billionaire founder of Vast)

Equipment and propulsion: For their upcoming Vestri mission, Safran Defense & Space will provide two EPS X00 electric propulsion systems (each comprising a PPS X00 thruster, power processing unit, and fluid management system). AstroForge now builds its spacecraft in-house after early outsourcing to OrbAstro failed.

Mission history:

Brokkr-1 (April 2023): A 6U cubesat launched on SpaceX Falcon 9 Transporter-7. Purpose: demonstrate metal refinery tech in orbit. The magnetic field from the refining system interfered with active attitude control, degrading pointing and communications. Solar arrays eventually deployed (September 2023), and telemetry could be downlinked, but AstroForge was never able to close the command uplink needed to activate the refinery payload. Last contact was May 2024.

Odin (Feb 2025): A 100 kg spacecraft launched as a rideshare on Intuitive Machines’ IM-2 mission via Falcon 9. Goal: flyby of near-Earth asteroid 2022 OB5. Built in-house in 212 days after the original OrbAstro-built version failed vibration testing. Cost: less than $7M. Declared lost on March 6, 2025 after failure to establish sustained communications. Initial comms were hampered by ground-station issues; ultimate loss could involve attitude, power, or deployment problems on the spacecraft side. Root cause was not definitively established.

Vestri (target window: 2026, possibly slipping to early 2027): A 200 kg spacecraft intended to travel to the same target asteroid and directly characterize its composition. Uses Safran electric propulsion. Planned to launch with Intuitive Machines’ IM-3 mission. Public sources vary on exact timeline and mission profile (some describe docking, others describe landing legs); treat the launch window and approach as provisional until a final mission statement is published. If it reaches the asteroid, it would be the first private spacecraft to rendezvous with a body outside the Earth-Moon system.

CEO Matt Gialich’s approach: “We’re going to mine asteroids or go bankrupt, and we’re going to probably figure that out in the next five years.”

Progress: Further along than anyone else in terms of actual flight hardware in deep space. But 2 missions have failed, and they haven’t demonstrated mining, refining, or return of any material. Still firmly in the prospecting phase.

2. Karman+

Target: Water from carbonaceous near-Earth asteroids, for in-orbit refueling

Founded: 2022 by Teun van den Dries (CEO, serial entrepreneur) and Daynan Crull (Mission Architect, technology strategist), headquartered in Denver, Colorado with roots in the Netherlands

Team size: ~29 employees

Total funding: $20M seed round (PitchBook lists $46.5M total)

Key investors: Plural (London), Hummingbird Ventures (Antwerp), HCVC (Paris), Kevin Mahaffey (Lookout founder), Climate Capital, Norrsken VC

Technical approach:

“COTS+” strategy: Adapting commercial off-the-shelf components from other industries, testing and qualifying them for space. Goal is to keep mission budgets under $10M per mission (vs. $1B+ for NASA asteroid missions).

Autonomous navigation: Developing optical navigation (”beacon nav”) for interplanetary cruise

Mining hardware: Building zero-gravity mining equipment for regolith excavation at kilogram scale

Extraction method: Excavate regolith, extract water, which can be used directly or decomposed into hydrogen and oxygen for propellant

First mission: “High Frontier” technology demonstration, targeting 2027 launch. Will attempt to rendezvous with a near-Earth asteroid and excavate regolith at kilogram scale.

Status (Q3 2025): Parts and components ordered; going through rapid design iterations with full-scale engineering model builds.

Market thesis: In-space refueling could be worth single-digit billions of dollars per year. Lowering satellite refueling costs by up to 10x compared to Earth-launched fuel. Later-stage plans include extracting rare metals and contributing to in-space manufacturing.

Progress: Earlier-stage than AstroForge; no flight heritage yet. But pursuing the arguably more plausible first market. Their cost targets are aggressive.

3. TransAstra

Target: Water and volatiles from asteroids using concentrated sunlight

Founded: 2015 by Dr. Joel Sercel (CEO), based in Los Angeles. Sercel spent 14 years at NASA’s Jet Propulsion Laboratory, taught at Caltech for 12 years, led conception of the NSTAR ion propulsion system (used on the Dawn spacecraft), and was the founding CTO of Momentus. He holds 14 patents pending in space resources technology.

Team: Partnered with Prof. Robert Jedicke (University of Hawaii) and researchers at the Colorado School of Mines Center for Space Resources (Angel Abbud-Madrid, Chris Dreyer)

Funding: Combination of private investment plus NASA grants and contracts. Six NASA NIAC fellowships (including one of the first two NIAC Phase 3 awards ever selected). Also won an $850K SBIR Phase 2 contract for inflatable capture bag development.

Core technologies:

Optical Mining™ (patented): Uses concentrated sunlight via deployable mirrors to heat asteroid material inside an inflatable containment bag, fracturing rock and driving off volatiles, which are captured and condensed. Tested at White Sands Missile Range solar furnace on actual meteorite samples.

Omnivore™ engine: A solar thermal rocket that can run on water, ammonia, hydrogen, or other propellants, designed for fuel-flexible in-space operations.

Sutter™ telescope technology: Synthetic tracking system claimed to be 300,000x more effective at finding dark moving objects than conventional telescopes. Won a DoD grant for space situational awareness applications.

Worker Bee space tug: In development for satellite repositioning using solar thermal propulsion. TransAstra has contracts and studies for the concept, but it is not yet flying routine commercial missions.

Architecture (Apis): The full concept envisions harvesting up to 100 metric tons of water from a single near-Earth asteroid and delivering it to lunar orbit or other depot locations, all from a single Falcon 9 launch.

Progress: The deepest R&D portfolio and the most experienced founder of the three companies. But further from commercial execution than AstroForge. TransAstra is pursuing near-term revenue from space tug and debris capture contracts while developing the longer-term mining architecture. Think of them as building the enabling infrastructure rather than going straight for the ore.

The Dead Companies

The two biggest names from the 2010s asteroid mining hype cycle are gone:

Planetary Resources (founded 2010, backed by Larry Page, Eric Schmidt, James Cameron): Acquired by blockchain company ConsenSys in 2018. Mining ambitions abandoned.

Deep Space Industries (founded 2013): Acquired by Bradford Space in 2019. Pivoted entirely to propulsion and spacecraft technology.

Is SpaceX or Blue Origin trying to mine asteroids?

SpaceX: No. No public asteroid mining program. SpaceX is an enabler and launch provider. AstroForge’s missions flew on Falcon 9. Their strategic focus is settlement infrastructure. SpaceX is prioritizing building a “self-growing city” on the Moon. Running a mining and commodities business is a completely different priority stack.

If a mature in-space economy develops where propellant is the bottleneck, SpaceX might get involved, but they’d more likely buy propellant from a specialist or focus on lunar/Martian ISRU rather than chasing asteroids.

Blue Origin: Not really. Blue Origin discusses building “space mining robots and systems” in the context of ISRU capability development. That’s building enabling technologies, not pursuing asteroid mining as a revenue line.

Who will do it first? Most likely a specialist startup with a focused architecture and potentially a government anchor customer. The big launch companies fit as enablers, not miners.

How close is any company to mining asteroids?

A milestone ladder for readiness:

Reach the asteroid reliably

Rendezvous or flyby imaging (prospecting)

Touchdown, docking, or anchoring

Excavate material in microgravity

Process/refine (separate metal, extract water)

Deliver product (to Earth or an in-space customer)

Repeat economically

Private companies are mostly between steps 1 and 3, still struggling to prove parts of 4 through 6.

For context on how hard “bring stuff back” is even for governments with billion-dollar budgets:

Missions:

NASA OSIRIS-REx (Sept 2023)

Asteroid: Bennu

Returned: 121.6 grams

Cost: ~$1.16B

JAXA Hayabusa2 (2019)

Asteroid: Ryugu

Returned: 5.4 grams

Cost: ~$150M

Those are scientific sample returns, not mining, but they illustrate the gap between “visit an asteroid” and “move industrial quantities of material.”

How many asteroids are close enough to Earth to mine?

“Close enough” isn’t about how near an asteroid passes Earth.

You need to think about whether you can match its orbit with a practical amount of delta-v (the velocity change your spacecraft needs) within reasonable mission timelines.

~39,123 total discovered near-Earth asteroids as of December 2025. Most aren’t economically reachable (high delta-v, bad launch windows, too small, spinning too fast, uncertain composition).

~6,294 are “NHATS-accessible” per NASA/JPL’s Near-Earth Object Human Space Flight Accessible Targets Study, meaning they have at least one viable round-trip trajectory. About 16% of known NEAs.

The “really easy” targets are rare. A 2015 NASA paper found only 580 NEAs reachable for less delta-v than a lunar surface round-trip (~9 km/s), and just 49 for less than a low lunar orbit round-trip (~5 km/s).

Many good targets haven’t been found yet. NASA estimates ~14,000 asteroids of 140m+ remain undiscovered. NEO Surveyor, launching no earlier than September 2027, is modeled to discover on the order of 200,000-300,000 new NEOs based on population models and survey simulations, though actual yield will depend on mission performance and survey duration.

Net: Tens of thousands of NEAs exist. Thousands are theoretically accessible. Dozens to low hundreds are plausibly economically accessible with good launch windows and workable physical properties, and many of those may still be undiscovered.

How will companies mine asteroids?

Step 1: Finding Targets

Companies start from catalogs of known near-Earth objects:

NASA’s NEO Observations Program funds discovery and orbit refinement

Ground-based optical surveys like the Catalina Sky Survey do most of the initial detection

JPL’s CNEOS turns detections into tracked objects with refined orbits

Infrared surveys catch dark asteroids invisible in visible light. NEOWISE (decommissioned August 2024) was a key survey; NEO Surveyor is its planned successor

From Earth, spectroscopy and albedo measurements give rough composition estimates. But the data is imperfect. That’s why prospecting missions (flybys or rendezvous) come first: you need to confirm composition and mechanical properties before committing hundreds of millions to a mining mission.

Step 2: Getting There

This is non-trivial for several reasons:

Targets are tiny and irregular, often spinning or tumbling

Gravity is essentially zero. Touching the surface can bounce you away (OSIRIS-REx experienced this)

Navigation is autonomous. Communication delays grow with distance, so the spacecraft must make its own decisions using optical guidance

Launch windows are constrained. You need the right orbital alignment, and windows may only open every few years for a given target

Step 3: Anchoring or Containment

Two broad strategies:

Anchor to the surface: Drills, harpoons, anchors, or nets to grip the asteroid. Difficult because surface properties are unknown until arrival, and there’s no gravity to help hold anything down.

Enclose the body: Wrap the asteroid in an inflatable bag and work inside containment. This is TransAstra’s approach. NASA studied a related concept in the (canceled) Asteroid Redirect Robotic Mission: capture a multi-ton boulder and redirect it to lunar orbit.

Step 4: Extraction

Water/volatiles (the nearer-term product):

Heat regolith in a sealed container, capture released vapor, condense it

TransAstra’s optical mining uses concentrated sunlight via deployable mirrors inside a containment bag

Karman+ is developing purpose-built zero-gravity excavation equipment and plans solar-thermal or microwave heating methods

Metals (harder, longer-term):

Shipping raw ore means paying to transport a lot of waste mass

Practical approaches require at least partial beneficiation in space: magnetic separation, melting, electro-refining

Each processing step adds mass, power requirements, thermal control complexity, and failure modes

The more you refine in space, the more your spacecraft becomes an industrial plant, which is a core tension in mission design

Step 5: Delivery

Option A, deliver in space (water to a depot orbit): No reentry system required. Serve a space customer. Electric propulsion tug hauls product to the most valuable orbital location. This is the cleaner near-term path, if customers exist.

Option B, return to Earth (metals): You don’t return the whole asteroid (planetary defense nightmare, regulatory impossibility). You return small, controlled capsules. The most sensible architecture:

Process in space to concentrate value and dump waste (tailings)

Return only high-value mass (ingots or concentrate)

Finish refining on Earth where industrial infrastructure is mature

What’s the potential payday?

Depends if precious metals or water/propellant, the amounts you extract, and the specifics (i.e. amounts/composition of precious metals).

Path A: Returning Precious Metals to Earth

Using platinum spot pricing from Feb 10, 2026 (~$2,083/troy oz), and palladium (~$56K/kg):

These numbers are misleading without context:

Values assume refined metal, not raw regolith. Extraction yields will be far less than 100%.

A lean deep-space mining mission might cost $200M all-in. Break-even platinum mass: ~3,000 kg (3 tonnes). That’s an enormous quantity of refined product to return, especially early in the learning curve.

The numbers ignore extraction yield losses, microgravity refining complexity, return capsule and recovery costs, and insurance against total mission loss.

Market impact: Global platinum mine supply was ~5,766 koz in 2024 (~179 metric tons from mining alone; total supply including recycling was ~7,293 koz or ~227 tonnes).

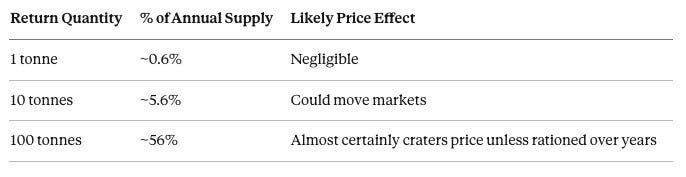

1 ton: ~0.6% of annual supply

10 tons: ~5.6% of annual supply

100 tons: ~56% of annual supply

So if a mining company were to extract and return 100 tons of platinum, they’d completely tank the price of platinum on Earth unless they slow-rolled sales over a period of many years (abundant supply = lower value; scarce supply = higher value).

The “this asteroid is worth $10 trillion” headlines are technically true and practically meaningless. Value does not equal realizable profit.

Path B: Selling Water/Propellant in Space

The payday here is tied to avoided launch cost, not Earth commodity prices.

One NASA reference benchmarks Falcon 9 delivery at ~$2,940/kg to LEO. If you can deliver asteroid water to a useful orbit for less, you have a business.

For harder-to-reach destinations (cislunar space, high-energy orbits, lunar vicinity), Earth-launched delivery costs are much higher, and the value of locally sourced propellant increases proportionally.

Early commercially meaningful deliveries would likely be hundreds of kg to a few tonnes. At $1,000-$5,000/kg delivered (location-dependent), that’s $0.1M-$25M revenue per delivery. You need repeatability and scaling for this to become a real business.

The catch: The entire business case depends on a real in-space refueling market materializing. That requires sustained cislunar activity (multiple lunar missions per year, orbital depots, tugs, standards for propellant transfer). Without demand, even cheap asteroid water has no ROI.

Does the ROI math work? (Biz model sustainability)

Significant ROI = repeatable commercial operations with large cumulative profit (order of $1B+) or equity-style returns that clearly clear “cool demo” status.

Short answer: Yes, a business can plausibly make significant ROI from asteroid mining, but most likely in the “sell water/propellant in space” lane, and not near-term. The classic “bring back platinum and get rich” lane is much less likely to work.

Economics of Earth-Return Metals

The cost stack for a “metals-return mission” includes: spacecraft development, launch, deep-space operations, autonomous mining hardware, in-space refining equipment, return capsule development, Earth reentry and recovery, ground-based final refining, and insurance.

With current technology and cost structures, breaking even requires returning multi-ton quantities of concentrated PGMs per mission; no one has demonstrated returning even grams commercially.

Even if you solve the engineering, you hit the market problem: large new supply pushes prices down.

WPIC reports total global platinum supply (mine + recycling) of ~7.293 million oz in 2024 (about 227 tonnes). If you ever return “real” tonnage, you start pushing the price against yourself unless throttled carefully.

And reliability remains a fundamental problem. Even government sample return is still tiny and expensive (OSIRIS-REx returned 121.6 grams after a $1.16B program).

Private deep-space startups still lose missions to basic ops risk: AstroForge’s Odin ran into severe comms/ops issues, exactly the kind of thing that destroys the economics until reliability becomes routine.

Refining (i.e. beneficiation) in microgravity adds mass, power, thermal management, autonomy requirements, and failure modes. If you don’t refine in space, you pay to return waste.

When could it work? If (1) mission costs fall dramatically (possibly through reusable deep-space architecture and learning-curve effects) + (2) a company can reliably return multi-ton quantities + (3) they meter supply to avoid crashing the market. Metals-to-Earth could happen as small “boutique returns” (kg-scale) for a long time, but that’s not significant ROI.

Economics of In-Space Water

Plausible, but conditional.

Water/propellant is valuable because it avoids Earth launch and transport.

You aren’t competing with terrestrial mining at all. You just need to beat the delivered cost to the customer’s orbit. That’s a different and more favorable competitive dynamic.

The unit economics are potentially favorable: water is enormously expensive to launch from Earth to useful orbits, and carbonaceous asteroids contain it in abundance.

There are thousands of “accessible” NEAs in mission-design terms, so targets exist; the difficulty is characterization, extraction, and reliable operations.

If you can build a reusable mining tug that visits low-delta-v asteroids and delivers water to orbital depots repeatedly, the per-kg cost could undercut Earth-launched alternatives, especially for harder-to-reach destinations (cislunar space, high-energy orbits) where launch costs multiply.

What has to go right:

The cislunar economy has to materialize (multiple lunar missions per year, commercial stations, depots)

Orbital refueling infrastructure and standards have to be developed

Someone has to prove the extraction technology works reliably in microgravity

The mining tug architecture has to be reusable enough to amortize development costs

The gating factor is demand. If there isn’t a sustained cislunar logistics market (depots, tugs, frequent lunar ops), asteroid water has no buyer.

Karman+ is betting on this path, with mission budgets targeted under $10M and a COTS+ approach to keep costs low, aiming at customer missions expected in 2027. If the refueling market reaches even low single-digit billions per year (their target), there’s room for positive unit economics. But the market doesn’t exist yet.

Will anyone generate high ROI? (GPT-5.2 Prediction)

I had ChatGPT’s 5.2-Pro/High speculate on odds. I would likely assign higher odds (with equally low confidence) given technological progress in space technology + AI + robotics, but maybe I’m slightly over-optimistic.

1. In-Space Water/Propellant Profitable

2035: ~5% odds (low confidence)

2045: ~15% odds (low-medium confidence)

2055: ~25% odds (low confidence)

Rationale (the most plausible path to significant ROI):

Water/propellant value comes from avoiding Earth launch + transport, not from competing with terrestrial commodity markets

Multiple teams are explicitly building toward water extraction demos

Thousands of accessible NEAs exist as targets

The gating factor is demand, not physics

2. Earth-Return Metals (PGMs) Profitable

2045: ~3% odds (low confidence)

2055: ~7% odds (low confidence)

2070: ~10% odds (very low confidence)

Why such low odds?

Government sample return is still tiny and expensive after billions spent

Private deep-space ops are still failure-prone at the most basic level (comms, navigation, power)

Market depth is a real constraint (~227 tonnes of total global platinum supply per year including recycling; ~179 tonnes from mining alone)

In-space refining adds enormous complexity; skipping it means paying to return waste

Even if technically successful, large returns push prices against you

3. Technical Mining Demo (extract 10-100+ kg)

Timeline: 2030-2040

Probability: ~60%

Confidence: Medium

Rationale: Core ingredients exist in pieces (rendezvous, sampling, return capsules, propulsion, autonomy). Can be government-supported or subsidized. Growing catalog of accessible targets and falling launch costs help.

The Realistic ROI Playbook

If significant ROI ever happens, it almost certainly follows this sequence:

Prospecting: Cheap rendezvous + close imaging + basic composition checks, done repeatedly across multiple targets

Containment/anchoring that works on small, spinning bodies in microgravity

Simple extraction first (water/volatiles), not complex metallurgy

Sell in-space to a depot or orbital customer, not back to Earth

Scale via repetition (many identical tugs) rather than one “hero mission”

This gets you away from Earth commodity markets entirely and into a logistics business. The company that succeeds looks more like a propellant delivery service than a mining company.

What would increase the odds?

A clear signal that the in-space refueling market is real and growing (multiple depots, routine tanker demand, NASA or commercial anchor customers)

Demonstrated “extract + store + deliver” at meaningful scale (even hundreds of kg), done more than once

Improved discovery and characterization pipeline (NEO Surveyor is scheduled no earlier than Sept 2027; while it’s planetary defense oriented, better catalogs help everyone)

Falling mission costs combined with rising spacecraft autonomy and reliability

Starship or similar next-gen heavy lift making deep-space missions dramatically cheaper to launch

Implications of asteroid mining success

If any commercial Earth-return happens in the next couple decades, expect a progression:

Grams to kilograms: Proof of capability. Negligible market effect.

Tens of kilograms: Still negligible market effect.

1 tonne of platinum (~$67M at current pricing): ~0.6% of annual mine supply. Probably not a market shock.

10 tonnes: ~5.6% of annual supply. Could start moving price, especially if dumped quickly.

100 tonnes: ~56% of annual supply. Almost certainly craters the price unless rationed across years.

The smarter play is likely selling in small, controlled batches, or targeting specialty applications where small quantities of ultra-pure space-refined PGMs command premium pricing… unless it’s so cost-efficient to mine that you just want to offload and keep accelerating.

Milestones to Track

If you want to gauge whether asteroid mining is getting real:

Repeated successful rendezvous + sustained comms with tiny targets (startup-grade spacecraft)

Demonstrated anchoring or containment that survives weeks to months

Demonstrated extraction of a measurable quantity (even grams to kg)

Delivery to a customer location (depot orbit) or Earth return of a meaningful payload

A second flight that repeats. This would be where economics start to exist.

Right now, no private company has cleared milestone 2. AstroForge’s Vestri mission (targeting 2026-2027) is attempting to reach milestone 2-3. Karman+’s High Frontier (2027) targets milestone 3.

Why most companies will quit asteroid mining (even with better tech)

“Technology improves over time” is true but insufficient. It doesn’t imply the same companies survive long enough to cash in, and it doesn’t imply asteroid mining becomes the best way to get resources.

A more accurate rule: Tech advances make it feasible (increases the chance someone does it), advances don’t guarantee profits (most early entrants still fail), and advances change the game (sometimes the winning play becomes lunar ISRU, recycling, or in-space manufacturing rather than asteroid-to-Earth commodities).

Time-to-revenue mismatch. Deep-space hardware cycles are long, failures are common, and “mining” requires multiple stacked breakthroughs (rendezvous, anchor, extract, store, deliver, repeat). Venture funding usually wants credible revenue paths inside 5-10 years. Many teams run out of runway before the inflection point arrives.

Reliability is the real wall. A single comms/nav/thermal failure can zero out an entire mission. Until reliability becomes “boring,” the expected value stays ugly. AstroForge’s Odin debrief is exactly the kind of mundane operational failure (comms, ground stations, timing) that wipes out a whole mission’s economics.

Demand might not show up. The best near-term product is in-space consumables (water/propellant/shielding mass). If the cislunar economy doesn’t scale, there’s no market regardless of how good your mining tech is.

Even if it becomes possible, it may not be profitable. “More resources exist” doesn’t mean a company earns outsized profits. If supply becomes easier, prices drop, margins compress, and the value accrues to downstream users, not the miner.

Pivots are rational. Teams often spin the tech into nearer markets: propulsion, autonomy, robotics, satellite servicing, lunar ISRU, defense contracts. That’s not “giving up.” It’s harvesting the only bankable portion of the stack. This is exactly what happened to Deep Space Industries (pivoted to propulsion, acquired by Bradford Space) and Planetary Resources (acquired by ConsenSys after funding trouble).

Will the current crop of mining companies survive?

An estimate by ChatGPT.

Base-rate odds for the current asteroid mining startup cohort by 2035.

~60-70%: Most “asteroid mining” startups either exit or pivot into adjacent businesses (propulsion, robotics, lunar ISRU, software, defense contracts)

~20-30%: One or two remain active but are still largely in demo/prospecting mode (not large profits)

~10%: At least one is doing repeatable commercial deliveries (most likely water/volatiles to an in-space customer)

Confidence: Medium on “lots of exits/pivots,” low on exact split.

Why are companies even trying with such low odds?

Asymmetric bet: Low probability, very large payoff, plus a bunch of partial wins that still monetize.

Power-law payoff. If you’re first to reliable extraction and delivery, you’re not just selling “ore.” You could control a logistics chokepoint for a future space economy.

You don’t need the full endgame to win. Even if “asteroid mining” fails, they can still create valuable spinouts: rendezvous/nav/autonomy stacks, anchoring/containment hardware, thermal extraction systems, in-space material handling. Those can sell into lunar, defense, satellite servicing, and tug markets.

Marketing and fundraising dynamics. “Mining asteroids” is an easy narrative to raise capital on compared to “we’re building an anchoring/containment system for small bodies.”

They’re betting the demand side turns on. If depots/tugs/lunar cadence ramps up, in-space consumables can become strategically valuable. Karman+ is making that demand bet explicitly.

Learning curve and iteration. The first few missions are expected to fail. They’re trying to survive long enough to get to “boring reliability,” which is when economics can start to exist.

The Wave Pattern

What you get is waves, not a single linear progression:

Wave forms (startups pitch asteroid mining, raise capital)

Wave dies (most fold or pivot because near-term ROI isn’t there)

Costs fall, demand rises, tech improves

New wave forms (often with the same pitch, slightly better enabling conditions)

You’ve already seen this once with Planetary Resources and Deep Space Industries. The current cohort (AstroForge, Karman+, TransAstra) is wave two.

Most will likely exit or pivot. The category will persist because option value, tech spillover, and the expanding target catalog keep drawing new entrants.

Does progress on Earth make asteroid mining unnecessary?

It can, especially for metals-to-Earth; Earth will also get better over the same timeframe.

Automation and electrification lower mining operating costs.

Recycling and better separation techniques improve effective supply.

Substitution changes demand (batteries and catalysts can shift away from specific scarce inputs).

Politics and environmental regulation can push costs up or drive investment into cleaner extraction methods.

The net effect is uncertain, but it’s not one-directional.

The competition isn’t “2026 Earth mining vs. 2050 asteroid mining” — it’s 2050 Earth mining vs. 2050 space mining.

If humanity is capable of industrial asteroid mining, it’s also likely capable of very efficient terrestrial mining, recycling, and substitution, and that can keep commodity prices low enough to kill asteroid-to-Earth margins.

Where asteroid mining still makes sense as both sides improve:

When the customer is already in space.

Water/propellant/shielding mass for cislunar logistics and feedstock for in-space manufacturing (once that exists) don’t compete with a mine in South Africa.

They compete with the delivered cost of launching mass from Earth to where it’s needed; a completely different competitive dynamic that improves with scale rather than degrading.

Will robots do the asteroid mining?

Yes, but probably not the robots you’re imagining.

Robots will almost certainly do most of it, but “humanoid miners” (biped, human-shaped robots walking around asteroids) may not be the obvious endgame.

Humanoid form factors are wrong for asteroids: Asteroids are the worst possible environment for a biped. Near-zero gravity plus rubble surfaces means walking is basically meaningless; you need anchors, tethers, and winches, not legs. Regolith is abrasive and electrostatically clingy, making humanoid joints and hands failure magnets. Radiation, thermal swings, and long-duration autonomy requirements favor simple, hardened mechanisms with few moving parts.

What the actual mining hardware looks like: Anchored multi-arm manipulators, tethered excavators/augers, bag/containment systems, thermal and microwave processing units, and small swarm inspectors for mapping and debris monitoring. The architecture is industrial, not anthropomorphic.

Where humanoids make sense: Maintenance and repair at a cislunar depot or processing hub, where the environment is designed around human-compatible interfaces (handrails, connectors, valves, standardized tool mounts). Handling unexpected failures where general dexterity matters. Teleoperation from nearby (lunar orbit, Gateway, depot) with low latency. In short: humanoids as the mechanics, not the mining rig. The mining hardware is specialized; the humanoid is the flexible fixer.

What robots don’t solve: Even perfect robots don’t eliminate the hard parts: delta-v and orbital logistics, power/thermal management, containment in microgravity, and the need for months-to-years of reliability without human rescue. Robots reduce labor cost and increase uptime, but the economics still hinge on delivered cost per kg and whether demand exists.

Most likely future architecture: Autonomous tug reaches the asteroid. Wrap, anchor, contain. Deploy purpose-built extraction and processing modules. Store product. Deliver to depot or return capsule. Dexterous robots (possibly humanoid-ish) service the depot and fix modules when things break.

When does “routine robotic asteroid mining” happen?

GPT-5.2-Pro gives its odds here as a forecast.

Humanoid robots as depot/station maintenance techs

2050: ~10% odds

2075: ~25% odds

2100: ~60% odds

Asteroid water/volatiles extraction as routine industrial activity

2050: ~5-10% odds

2075: ~20-30% odds

2100: ~35-55% odds

Metals-to-Earth as common business

2050: <5% odds

2075: ~5-10% odds

2100: ~5-15% odds

Humanoid depot maintenance comes first because servicing infrastructure in a controlled environment is where dexterity pays off. Asteroid extraction comes later because you need cheap/reliable deep-space ops, robust autonomy, and sustained demand. Metals-to-Earth may never become “common” because commodity markets, substitution, recycling, and price collapse dynamics fight you at every step.

Using the Moon as a Processing Hub?

A common question:

Why not capture an asteroid, bring it to the Moon, process it there with gravity and infrastructure, and ship refined product to Earth?

Version 1: Park a small asteroid or boulder in cislunar orbit and process it there.

This is the version NASA seriously studied. The Asteroid Redirect Mission (ARM) concept would capture a multi-ton boulder and move it into a stable lunar distant retrograde orbit (DRO) for repeated visits and processing.

Academic work has also shown a small subset of very tiny NEOs could be “retrieved” into Earth’s neighborhood with less than 500 m/s of delta-v using low-energy transfers.

Pros: Much shorter comm delays and easier ops than deep space, you can reuse infrastructure (tugs, power, processing rigs), you can fail/repair/iterate more like an industrial program.

Cons: You’re still in microgravity (so “mining like on Earth” isn’t solved), you import planetary defense and liability concerns (deliberately altering orbits), and it only works for small bodies.

Version 2: Land asteroid material on the lunar surface, process it on the Moon, then ship product to Earth.

This is physically possible but usually the wrong economic move. Landing is expensive (the Moon has no atmosphere, so you must spend propellant to land safely, unlike Earth where you get “free braking” via atmospheric reentry).

You’re hauling waste mass (if you bring raw ore/regolith to the Moon, you’re paying to move mostly not-the-valuable-stuff). You still need a return system to Earth (capsules, heat shields, recovery).

And if you already have lunar industrial infrastructure (power, robotics, processing plants, propellant), then mining the Moon itself (ice, oxygen, metals via something like Blue Origin’s Blue Alchemist) is often a nearer, simpler supply chain than importing asteroid feedstock.

Which version might work?

Plausible “Moon helps” pathway: Identify a small, low-delta-v near-Earth object, use a solar-electric tug to nudge it into a stable cislunar orbit (DRO or Lagrange vicinity), process it in orbit with reusable equipment, and return only concentrated product to Earth in small capsules. That’s a “cislunar processing hub,” not “drag a mountain to the Moon.”

Overall: Landing and hauling bulk mass tends to wreck economics unless you already have a mature lunar industrial base and you’re only transporting high-value concentrates. The Moon doesn’t automatically make asteroid mining easier; it mostly adds delta-v costs unless your architecture is specifically designed around cislunar orbit processing.

Long-Term Outlook: Asteroid Mining in 2100

The long-range outlook is path-dependent on whether a large cislunar economy actually forms. There’s no single “status quo” for the end of the century. The right way to frame it is as a scenario set.

Scenario A: Modest Space Economy (science + defense + limited industry)

Probability by 2100: ~35%

Space activity is big compared to today, but still not “industrial”

Resource use is mostly lunar ice/regolith ISRU for local ops; asteroid work is occasional and strategic

“Asteroid mining” exists mostly as government/strategic capability and niche commercial demos

Earth commodity markets are basically unaffected (no meaningful Earth-return flows)

Scenario B: Large Cislunar Economy (depots, tugs, habitats, lunar industry)

Probability by 2100: ~50%

The main space “mining” businesses are consumables and construction mass: water (life support, shielding, propellant feedstock), oxygen (oxidizer, life support), bulk mass for shielding/structures

Asteroids matter, but mainly as feedstock for in-space use: water-rich bodies for volatiles, metallic bodies for in-space metallurgy once automation is mature

Metals-to-Earth is still a niche, not the core. If any Earth return happens, it’s throttled, high-value, regulated, and small relative to global markets

The winners look like “space logistics suppliers,” not classic miners: a few operators with fleets of autonomous tugs and processing nodes near stable cislunar orbits, selling delivered mass in the right orbit

Scenario C: Inner Solar System Industrialization (very large-scale automation)

Probability by 2100: ~15%

Most heavy industry that can be moved off-Earth is moved off-Earth

Asteroid mining is routine and huge in tonnage, but almost all value is in-space manufacturing, not Earth commodity arbitrage

Earth becomes a “high-value surface” (data/biotech/culture/residential) while bulk materials and energy-intensive manufacturing happen in space

Earth markets for PGMs/metals are either mostly irrelevant (substitution/recycling/post-scarcity dynamics) or heavily managed to avoid destabilizing terrestrial economics

ROI Probabilities by 2100

No significant ROI; only demos + small gov programs: ~35% (low-medium)

Significant ROI from in-space consumables (water, oxygen, shielding mass): ~45% (low)

Significant ROI from metals-to-Earth (PGMs): ~10% (very low)

By 2150, the odds rise mainly because by then the question of whether space industry exists at scale has mostly been resolved one way or another.

In-space asteroid resources reach ~60-70% probability of significant ROI; metals-to-Earth reaches ~15-25% (very low confidence on both).

The big uncertainty across all timeframes is not “can we physically do it.” It’s whether the economic substrate (customers in space, infrastructure, legal/regulatory stability) actually matures.

Bottom Line: Asteroid Mining (as of 2026)

Significant ROI before ~2040: Unlikely.

Significant ROI by mid-century: Possible, but mostly via in-space water/propellant, not Earth-return metals.

Metals-to-Earth as a major profit engine: Long-shot. Could happen as small boutique returns for a long time, but $1B+ cumulative profit from PGM return is a ~3-10% probability through 2055. Earth-side mining, recycling, and substitution will also improve over the same period, keeping commodity prices low enough to squeeze asteroid-to-Earth margins.

Water/propellant for in-space use: The only version of asteroid mining with a plausible near-term path to significant ROI. The economics are cleaner, the engineering stack is shorter, and you’re selling something priced against avoided launch cost rather than competing with terrestrial mines. This is where the smart money is going (Karman+, TransAstra).

Most current companies will quit or pivot. The historical pattern and the base-rate expectation. The category will persist in waves: new entrants will form each time costs fall, targets improve, and demand signals strengthen. The capability will eventually be achieved. The question is when, and by whom, and whether anyone makes real money doing it or whether the value accrues to downstream users.

The “this asteroid is worth quadrillions” framing is technically true and commercially useless.

The real question is narrower: Can someone build a reusable spacecraft that extracts water from a low-delta-v carbonaceous asteroid and delivers it to a cislunar depot cheaper than launching it from Earth? That’s the version of asteroid mining that might actually happen first, and even that is probably 10-20 years out with single-digit-to-25% odds depending on how far out you look.